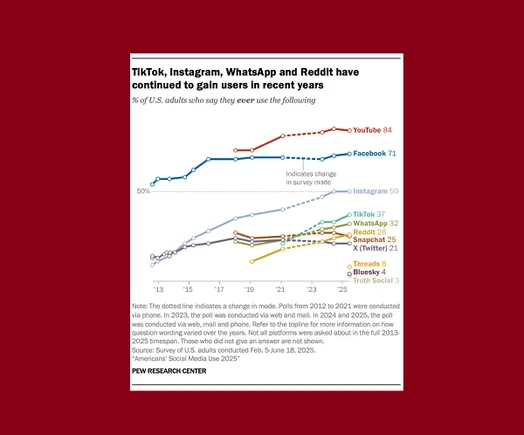

Pew Research surveyed 5,000 U.S. adults and found YouTube and Facebook lead in overall app reach, with 71% of respondents reporting they ever use Facebook; Threads registers about 8%, Bluesky 4%, and X 21%. The report also shows Instagram, Snapchat and TikTok dominate among younger users but emphasizes that the metrics ('ever use' and frequency of visits) do not measure time spent, limiting inferences about true engagement and advertising monetization.

Market structure: Dominant platforms with broad reach (scale owners of social/video supply) retain structural pricing power for high-quality ad inventory; expect CPM spreads to favor Alphabet (GOOGL) and Meta (META) over niche youth-focused apps, creating a bifurcated ad market where mid-tail sellers face margin compression of 200–500bps over 12–24 months. Cross-asset: a prolonged ad reallocation toward scale names supports credit spreads for large-cap ad-dependent issuers but raises downside gamma in equity options for smaller ad plays; FX/commodities impact immaterial. Risk assessment: Tail risks include rapid regulatory action (privacy/antitrust) that could force data-sharing limits within 6–18 months, and an advertising recession scenario (ad spend down >8% YoY) that would disproportionately hit small-cap ad-revenue-heavy names. Hidden dependencies include advertiser measurement shifts and Apple/OS privacy tweaks that can reduce effective CPMs by 5–15%; catalysts to watch are MAGNA ad forecasts, quarterly ad revenue beats/misses and any new privacy regulation in the next 90 days. Trade implications: Favor large-cap ad incumbents and ad-infrastructure names that capture reallocation (GOOGL, META, TTD) and underweight or hedge SNAP and PINS where monetization vs reach is weakest; expect relative performance divergence of 10–25% over 3–12 months. Use defined-risk options to express views (3–9 month spreads) and rotate 5–10% of equity cash into ad-tech exposure while trimming high-beta small caps. Contrarian angles: The market confuses reach with monetizable attention — consensus may overpay for youth-skewed platforms where time-spent and CPMs lag; historical parallel: incumbent consolidation after early multi-platform fragmentation (post-MySpace era) suggests durable winner-take-most dynamics. Unintended consequence: ad buyers chasing youth on niche apps could drive short-term CPM inflation but longer-term ROI downgrades, prompting rapid budget reversion back to scale platforms.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00