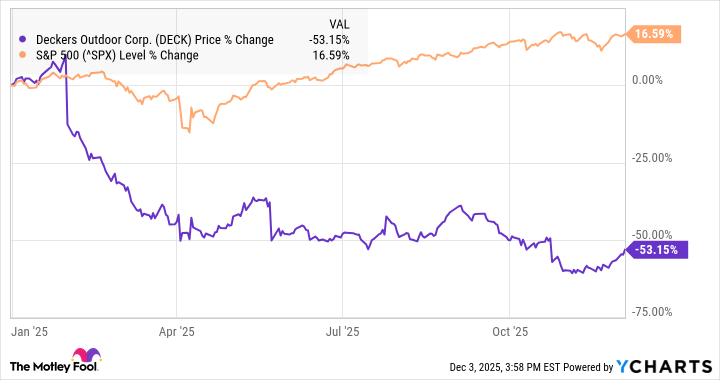

Deckers' 2025 performance deteriorated as fiscal Q2 revenue growth slowed to 9% YoY with U.S. sales up only 1.7% while international sales surged 29.3% and now represent over 40% of revenue. Management expects low‑teens Hoka growth and low‑to‑mid‑single‑digit UGG growth for the full year; gross margin ticked up to 56.2% from 55.9% and the stock is down ~53% YTD trading at ~14x earnings, implying valuation reflects meaningful downside but international strength and margin resilience could support a recovery if domestic demand stabilizes.

Market structure: Weak U.S. consumer demand (DECK domestic +1.7% vs international +29.3%) benefits premium, internationally-exposed brands (DECK/Hoka) and DTC channels while hurting mass-market retailers (TGT) and commoditized footwear makers. If DECK sustains gross margin ~56% (current 56.2%) it preserves pricing power and forces competitors into markdown-led share loss; a continued U.S. slump would compress industry volumes by mid-single digits next 12 months. Cross-asset: consumer stress tends to widen high-yield spreads (+50–150bp risk) and boost equity vol; a stronger USD would blunt reported international revenue growth, while stable commodity inputs would support gross margins. Risk assessment: Tail risks include tariff escalation adding >$50M of cost, abrupt China regulatory reversal, or a consumer recession driving U.S. sales down >5% and margins below 52%, any of which could trigger another 30–50% equity leg lower. Time horizons: immediate (days) - quarterly/holiday guidance; short-term (weeks–months) - Black Friday/holiday sell-through and tariff news; long-term (quarters–years) - European/China store rollouts and Hoka share gains. Hidden dependency: margin resilience currently relies on DTC mix; wholesale weakness could force promotional activity if DTC growth slows. Trade implications: Tactical: establish a phased 2–3% long in DECK (NYSE: DECK) using dollar-cost averaging: 1/3 now, 1/3 on a >5% pullback or P/E to 12, final 1/3 after two consecutive quarters with gross margin >=55% and international revenue growth >=20% YoY. Pair: long DECK vs short TGT (0.8:1 stock weight) to isolate premium-brand upside vs mass-retail downside until 1H2026 results; Options: buy 9–12 month DECK call spread (buy ATM, sell 25–35% OTM) sized to 0.5–1% portfolio to cap premium. Contrarian angles: The market may be overstating permanent domestic decline and underweighting DECK’s international runway—>40% revenue and Hoka low-teens guidance points to mid-teens total growth if U.S. stabilizes. Historical parallel: Crocs/UGG-style brand recoveries show durable margin recapture after an inventory reset; if gross margin stays >55% and U.S. comps recover to +3% in two consecutive quarters, upside could be 40–80% materially outperforming peers. Risk: if management lowers guidance or gross margin slips below 54%, close positions immediately.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment