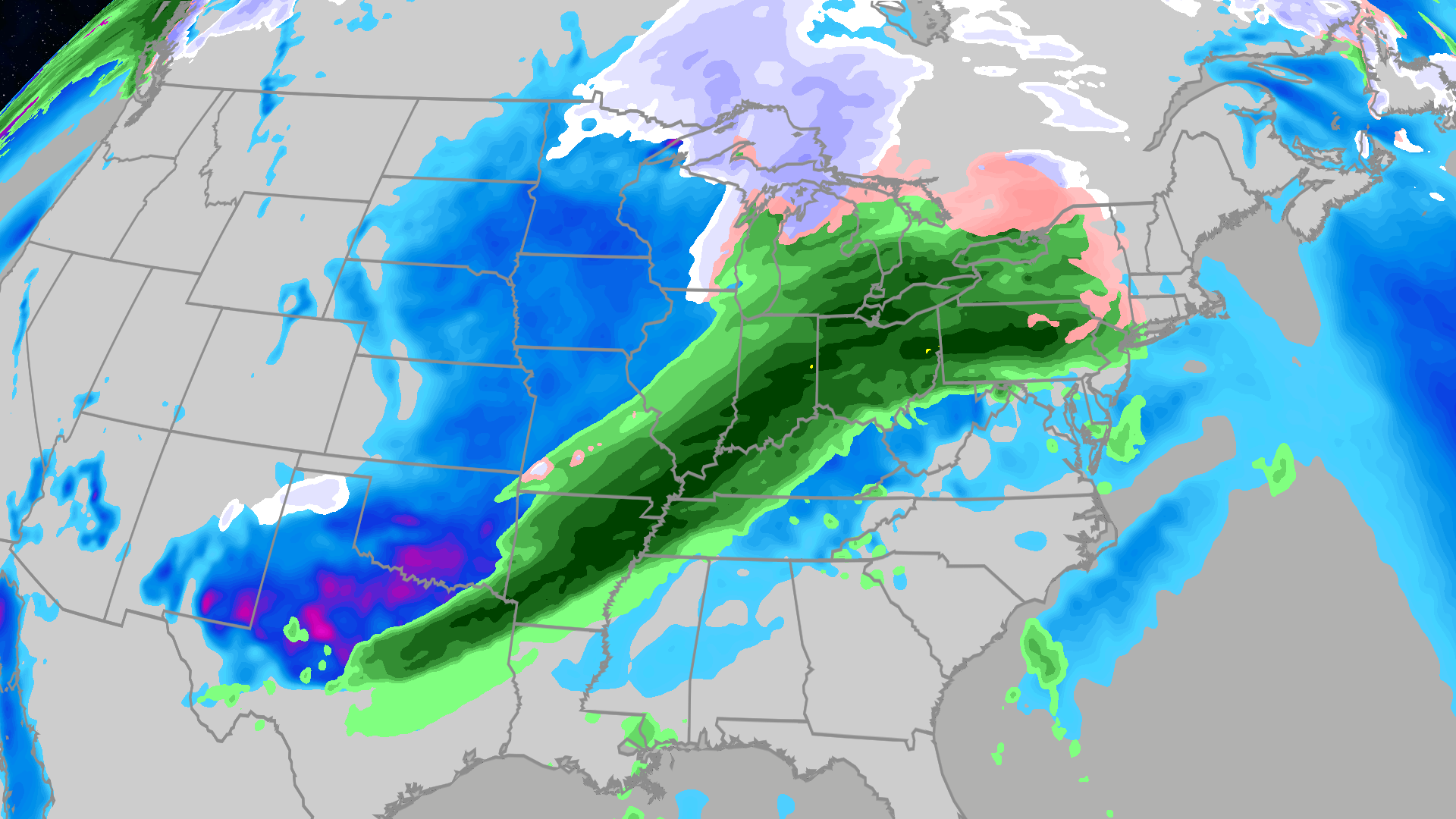

A sequence of winter storms will disrupt post-Christmas travel across the U.S.: Winter Storm Devin will push snow, sleet and freezing rain from the Great Lakes into the Northeast on Friday (ice accumulations around 0.25" possible in parts of central/western Pennsylvania and 5–8" of snow, isolated up to a foot, in warning areas), threatening significant flight delays and power outages at major Northeast hubs. A Pacific storm continues heavy rain and mountain snow in California and the Sierra, while Saturday brings quieter western weather but strong winds and lingering snow in the Rockies; Sunday a cold front spawns another storm across the Midwest, Great Lakes and Northeast with heavy lake-effect snow and the potential for severe thunderstorms and damaging winds from the Great Lakes to the northern Gulf Coast, posing near-term operational risks for airlines, ground transport and regional infrastructure.

Market structure: Near-term winners are ground-transport and energy exposures (car rental CAR, Hertz HTZ, short-dated natural gas) while hub-dependent legacy airlines (AAL, DAL, UAL) and Northeast hotels (MAR, HLT) face immediate revenue hits from cancellations and delays. Airport ops and integrators (AAL/UAL routes, UPS, FDX) will see concentrated operational risk because cancellations cascade through hub-and-spoke networks; expect 1–5% negative revenue disruption for large carriers over the next 7–14 days versus baseline holiday volumes. Risk assessment: Tail risks include multi-day airport closures or power outages in the ice-impacted I-95 corridor causing 5–10% incremental holiday revenue loss for carriers and meaningful rebooking costs for OTAs (BKNG, EXPE) — low probability but high impact in 48–72 hours. Immediate window (days): operational volatility and IV spikes; short-term (weeks): rebooking revenue shifts and gas/heating demand; long-term (quarters): limited structural change unless supply-chain or regulatory investigations follow catastrophic outages. Trade implications: Expect elevated options volatility on airlines and OTAs; implement short-dated protection or event-driven shorts on carriers (30–45 day puts) and buy short-dated NG call exposure (2–6 week) to capture heating-driven upside. Consider pair trades that long car-rentals (CAR) vs short OTAs (EXPE) for a 1–4 week horizon, and trim hotel exposure (MAR, HLT) into any 5–10% post-event pop. Contrarian angles: The market may overprice permanent harm — historical winter-storm selloffs tend to mean-revert within 1–3 weeks as rebookings and elevated fares restore revenue; implied vols can be overstated by 20–40%, creating opportunities for disciplined calendar/credit spreads. Unintended consequence: heavier lake-effect snow could boost industrial heating demand and short-term NG, supporting energy longs while pressuring consumer cyclical names tied to discretionary travel.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.30