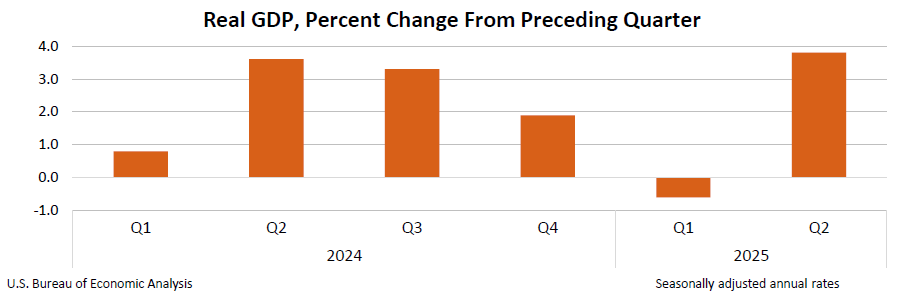

The U.S. economy expanded at a robust 3.8% annual rate in the second quarter of 2025, a significant upward revision from previous estimates and a strong rebound from the first quarter's 0.6% contraction. This growth was primarily fueled by increased consumer spending and a decrease in imports, though it was partly offset by reduced investment and exports. While the PCE price index saw a slight upward revision to 2.1%, corporate profits for Q2 were revised significantly lower, increasing by only $6.8 billion, a $58.7 billion downward adjustment from prior estimates.

The third estimate for U.S. economic activity in Q2 2025 reveals a robust 3.8% annualized growth in real GDP, a significant upward revision of 0.5 percentage points from the second estimate and a sharp reversal from the 0.6% contraction in Q1. This acceleration was primarily driven by an upwardly revised increase in consumer spending and a decrease in imports, which are a subtraction from the GDP calculation. The strength of domestic demand is further underscored by the 2.9% increase in real final sales to private domestic purchasers, which was revised up by a full percentage point. However, this top-line strength is sharply contrasted by a significant negative signal from corporate earnings. Profits from current production were revised downward by $58.7 billion, resulting in a muted increase of only $6.8 billion for the quarter. This divergence between strong GDP growth and weak corporate profitability, alongside a 1.0 percentage point downward revision to Real GDI, suggests that underlying economic health may be less vigorous than the headline GDP figure implies, potentially indicating margin pressure on corporations. Concurrently, inflation metrics were revised slightly higher, with the core PCE price index now at 2.6%, suggesting that inflationary pressures remain persistent.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.50