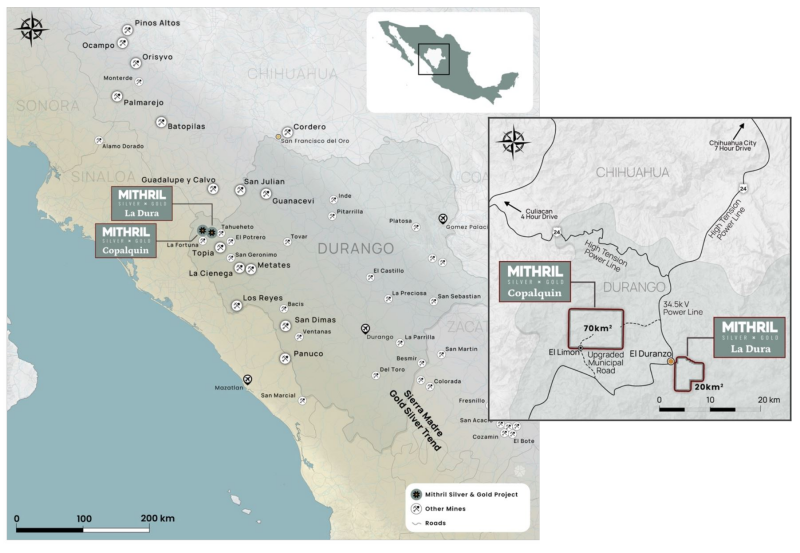

Mithril Silver & Gold has mobilized a third drill rig and outlined an expanded 2026 exploration program at its 100%‑owned Copalquin gold‑silver district in Durango, Mexico, planning ~25,000 m of drilling and up to three rigs in H1 2026. Near‑term programs include a 3,300 m first phase at Target 3 (near El Jabali, recent channel sampling up to 16 g/t Au and 1,275 g/t Ag), ~3,000 m at Target 1 ahead of a resource update (western step‑out hole 8.03 m @ 7.19 g/t Au, 260 g/t Ag) and ongoing follow‑up at Target 5 with strong early intercepts (e.g., 2.75 m @ 2.28 g/t Au, 500 g/t Ag). The company flagged significant assay lab delays (≈20 holes pending and 12 recently shipped) but plans district‑scale LiDAR and an aerial magnetic survey in Jan 2026 to refine targets and support resource expansion.

Market structure: Primary winners are Mithril (ASX:MTH / TSXV:MSG / OTCQB:MTIRF) and service providers (drill contractors, geophysics firms) if 2026 drilling confirms continuity; large producers and metal prices are effectively neutral because 25,000 m is too small to move gold/silver supply. Competitive dynamics favor juniors with district-scale epithermal systems in Mexico — a confirmed multi-million-ounce expansion would materially increase MTH’s M&A optionality versus peer juniors and could re-rate small-cap juniors (positive spill to GDXJ) without changing commodity pricing. Risk assessment: Key tail risks include persistent assay-lab bottlenecks (information vacuum), forced equity raises (dilution), regulatory/security events in Mexico, or negative metallurgical/continuity assays. Immediate (days/weeks): volatility around assay releases; short-term (1–6 months): cash burn from 3 rigs and 25,000 m program; long-term (6–36 months): resource updates, option payment US$10M by Aug 2028 and potential M&A. Hidden dependency: ALS backlog creates signaling risk — management can pace news and drilling to manage financing windows. Trade implications: Direct speculative play is small long equity in MTH sized 1–2% of portfolio with tranching tied to assay confirmations; hedge metal exposure by shorting GDXJ at ~0.5x notional to isolate asset-specific upside. Options: express convexity via 3–6 month GDXJ call spreads sized to 0.25–0.5% portfolio to capture junior re-rating on positive district-scale news. Entry: initiate now (small tranche); add on receipt of >10 pending assays within 30–90 days showing composite intercepts >=5 g/t AuEq across structural continuity; exit/trim on >50% rally or on financing >15% dilution. Contrarian angles: Consensus may underweight the risk of dilution and overestimate discovery continuity — positive assays can be priced for M&A premiums (historical small-cap takeovers often 40–100% premiums). Lab delays often precede staged newsflow; treat lack of assays >90 days as a negative signal. Conversely, if LiDAR/magnetics (Jan 2026) identify multiple drill-ready targets and assays confirm high-grade continuity, expect >2x re-rate in a 6–12 month window for MTH versus peers. Unintended consequence: three rigs accelerate cash burn and could force funding at sub-market prices if results disappoint.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.42