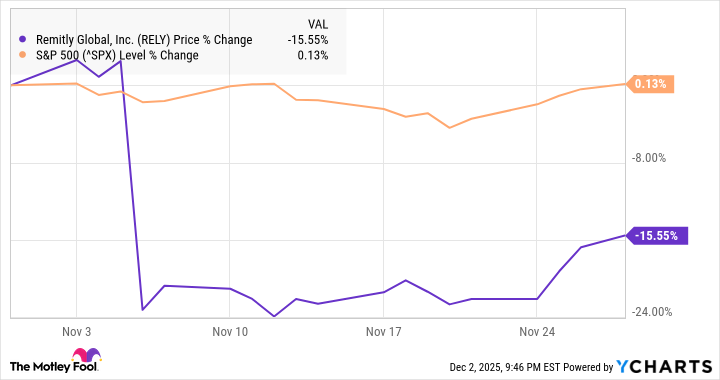

Remitly reported strong third-quarter results with active customers up 21% to 8.9 million, send volume up 35% to $19.5 billion and revenue rising 25% to $419.5 million (vs. $413.7M consensus); adjusted EBITDA grew 29% to $61.2 million. The stock plunged after management signaled slowing growth and increased credit risk, guiding fourth-quarter revenue of $426M–$428M (21% growth) below the $430.5M consensus; shares finished the month down ~16% and hit a 52-week low. Company highlights include product expansion (Remitly Business, Remitly One, stablecoins) and a full-year GAAP profit expectation, while valuation appears cheap at under 2x price-to-sales and ~12x expected EBITDA. The update matters for positioning due to the guidance-driven re-rating and credit exposure amid a weakening U.S. economy, even as long-term upside is cited from product initiatives and targeting higher-value senders.

Market structure: Remitly's combination of accelerating volume (+35% QoQ send volume) and lower take rates shifts value from per-transaction incumbents (WU, MGI) toward platform players who can monetize scale and ancillary finance (Remitly Business, stablecoins). Winners are digital-native rails and FX/crypto liquidity providers; losers are legacy cash-heavy branches and high-cost retail cash payout networks. Lower take rates pressure near-term revenue per dollar transferred, but higher volume and membership products can re-price unit economics if credit losses remain contained. Risk assessment: Key tail risks are regulatory (stablecoin/AML clampdowns), credit losses from BNPL-style features, and FX corridor dislocations if remittance demand contracts in a US recession. Immediate risk (days-weeks) is elevated implied volatility and potential further sell-offs around guidance; short-term (3–9 months) hinges on Q4 revenue vs. $426–428M guide and any net charge-off disclosure; long-term (12–36 months) depends on ability to hold EBITDA margins while growing customers ~15–25% annually. Trade implications: Given RELY trades <2x P/S and ~12x forward EBITDA, a measured long is warranted: tranche 2–3% portfolio exposure over 4–6 weeks, stop-loss if Q4 revenue < $425M or guidance for net charge-offs rises >100 bps. Pair trade: long RELY 2% vs short WU 1.5% (dollar-neutral) over 12–18 months to capture digital share gains. Options: buy a 9–12 month call spread equal to ~1% portfolio risk (buy lower strike, sell higher strike ~+40%/+80% from current) to define downside. Contrarian angles: The market is likely overstating permanent take-rate decline; product-led ARPU recovery and stablecoin-driven FX savings could lift EBITDA beyond consensus — a rerating to 18–24x EBITDA is plausible if growth stabilizes. Conversely, regulatory action on tokenized USD or material credit losses would rapidly de-rate the name, so size positions small and prefer defined-risk options or tight triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.28

Ticker Sentiment