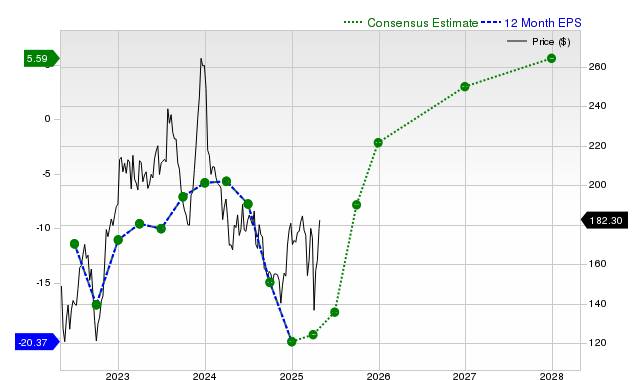

Boeing reported revenue of $23.27 billion in the last quarter (+30.4% YoY) and an EPS loss of $7.47 (vs. -$10.44 a year ago), with revenues beating the Zacks consensus by 6.09% while EPS missed by ~94%. Zacks shows mixed estimate momentum: the near-term consensus expects a $0.43 loss this quarter and a fiscal-year loss of $9.53 (estimates have been revised down in the last 30 days: -18.9% current quarter, -15.6% FY, -39.3% next FY), while next fiscal year consensus is $0.97; Zacks assigns Boeing a Rank #3 (Hold) and a Value Style Score of F. The data point to improving top-line recovery but continued earnings pressure and downward estimate revisions, suggesting cautious investor positioning rather than a clear buy or sell signal.

Market structure: Boeing is in a recovery but faces bifurcated winners — OEMs with stable production (Airbus/EADSY) gain share if Boeing delivery hiccups continue, while large commercial airlines and defense contractors (LMT, RTX) win from stable deliveries or increased defense budgets. The revenue trajectory (+30–43% YoY) signals demand is intact but margins and cash conversion are the choke points; expect pricing power on widebodies to remain weak for 6–18 months while narrowbody backlog supports volume. Risk assessment: Tail risks include a FAA/regulatory setback or large warranty litigation that could blow a 12-month recovery (low prob, high impact) and supplier-chain labor bottlenecks that push out deliveries. Near-term (days/weeks) equity moves will be driven by analyst estimate revisions and short-term delivery announcements; medium-term (3–12 months) by quarterlies and certification milestones; long-term (1–3 years) by margin normalization and defense contract timing. Trade implications: Direct equity exposure should be tactical and event-driven — prefer asymmetric option structures to buy optionality on a 6–12 month recovery while limiting downside. Relative-value: long Boeing exposure versus short highly levered suppliers (Spirit AeroSystems SPR) if production/quality headlines accelerate; rotate from tech growth (NVDA) into cyclicals only after two consecutive positive EPS revisions for BA. Cross-asset: a regulatory shock would widen BA credit spreads and equity implied vol — buy protection across both markets. Contrarian angle: Consensus focuses on EPS volatility; it underweights convertible economics of a large backlog turning into FCF once production stabilizes — a single quarter of sequential delivery acceleration (>+5% Q/Q) could force a rapid re-rating. The post-737 MAX precedent shows recoveries can take multiple years, so the market may be underpricing the pace of operational risk even as it overprices immediate binary outcomes.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.05

Ticker Sentiment