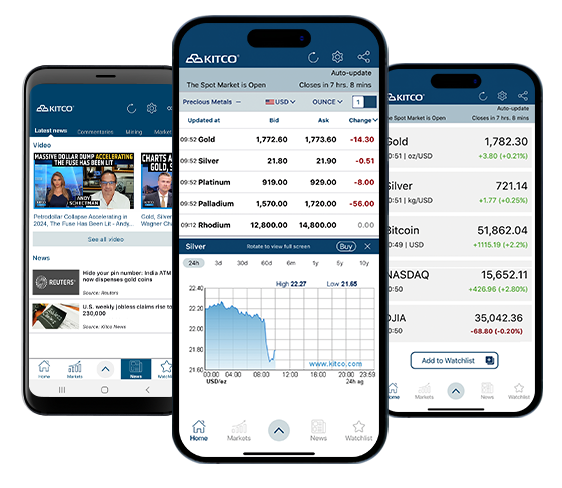

Global markets opened cautiously higher with S&P 500 futures +0.4% and Nasdaq futures +0.1% amid thin holiday volumes and record equity inflows (~$98bn last week). Key market movers: the Bank of Japan raised its policy rate to 0.75% (a 30-year high), pushing 10-year JGB yields to ~2.08% (+6bps) and sending the yen to record lows (¥184.92/euro; ¥157.37/dollar) under intervention watch. Safe-haven and commodity strength was pronounced—gold topped $4,400/oz and silver hit $69.44—while Brent rose to $61.60/bbl after U.S. actions against Venezuelan tankers; U.S. 10-year yields traded near 4.17%. Analysts warn extreme bullish sentiment from fund managers, adding risk of positioning-driven reversals.

Market structure: BOJ normalization (rate 0.75%, 10y JGB 2.08%) has bifurcated winners and losers — Japanese exporters (currency benefit) and commodities/gold (safe-haven/hedge) gain, while domestic bond holders and FX-sensitive importers suffer. Thin year-end liquidity (weekly equity flows $98bn) amplifies directional moves; intervention risk crystallizes around USD/JPY ~157.9 — a hard threshold that can create violent one- or two-way moves. Risk assessment: Near-term (days) volatility is elevated due to light volumes and BOJ minutes (Wed) plus a governor speech (Dec 25); short-term (weeks) tail risk is Tokyo intervention or sudden BOJ backtrack, medium-term (3-12 months) risk is policy divergence widening global rate dispersion. Hidden dependency: momentum/fund flows (BofA sentiment 8.5) mean a crowded long-equity/commodity position could flip quickly if US Jan labor/inflation surprise; catalytic triggers are BOJ communications, USD/JPY breaching 160, and additional tanker seizures impacting oil. Trade implications: Tactical plays should be asymmetric and capped — prefer defined-risk FX options (USD/JPY call spreads), selective long exposure to Japan exporters (EWJ, SONY, TM) sized 2–4% with JPY-hedge, and convexity trades into gold/silver (GLD/SLV call spreads) sized 1–3%. De-risk long-duration US fixed income (trim TLT) and consider 2s/10s steepener if 10y > 4.3% (buy steepener) given modest upward pressure on yields. Contrarian angles: Consensus equity/commodity flows look crowded and may be underpricing intervention and a rapid JPY reflation scenario — if Tokyo intervenes successfully, exporters’ FX tailwind collapses and safe-havens re-rate. Historical parallel: late-1990s/early-2000s BOJ repricing produced fast JPY rallies; hedge USD/JPY exposures and keep defined-risk protection ready to capture the reversal mispricing.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment