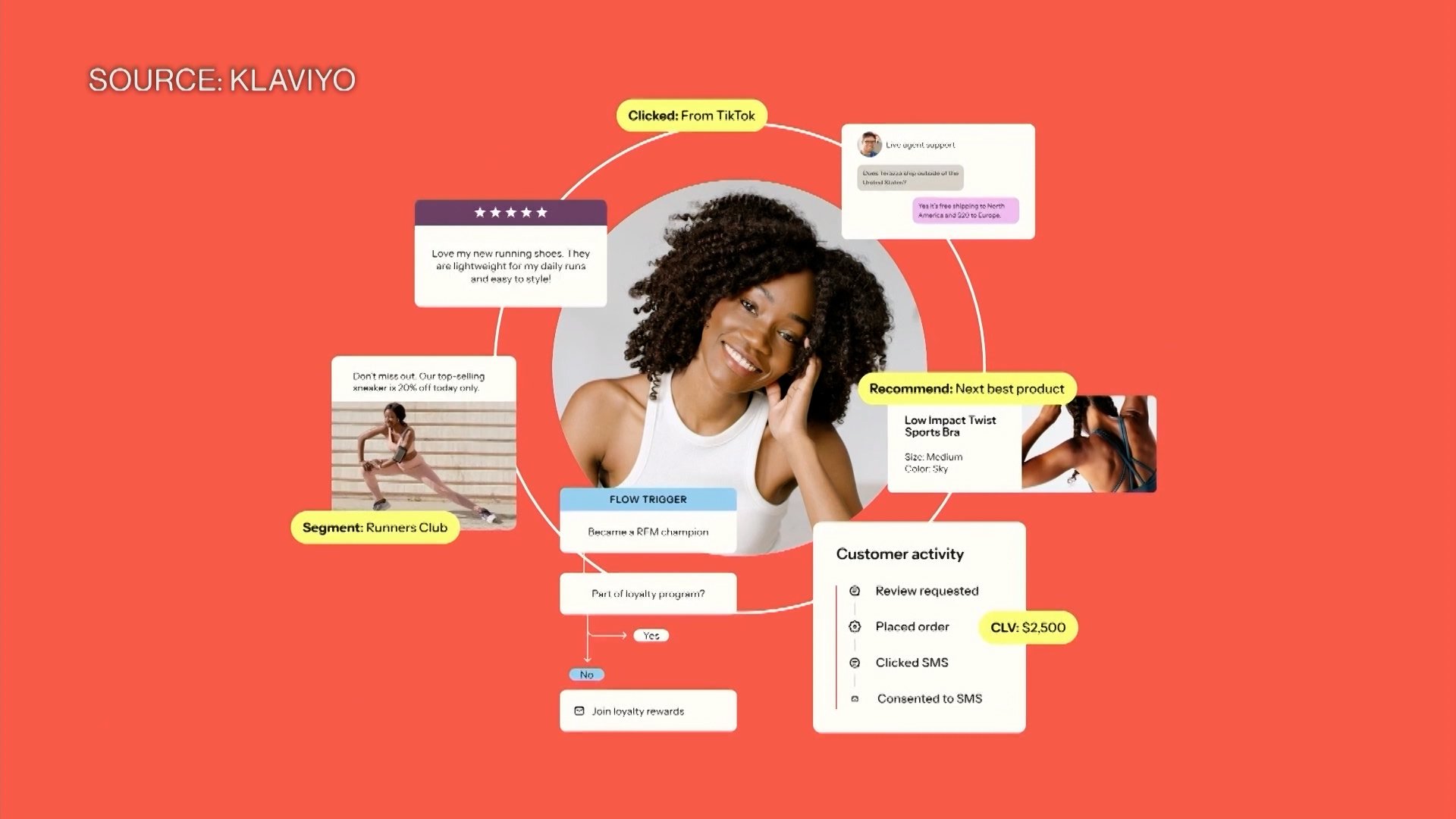

Klaviyo reported record Black Friday performance with over $1,000,000,000 in sales attributed to its platform (a ~25–26% increase) and roughly 20,000 merchant clients hitting their best single sales day; repeat buyers and engagement rose materially, with product views up 37% year‑over‑year. Health & beauty and apparel led category growth (~+12% each), while many retailers entered the season conservatively on tariff concerns, leaving inventories and promotional posture healthy and resulting in better‑than‑expected price elasticity; brands are increasingly using conversational AI for personalization and customer service. Analysts expect winners to be scale/value players (Walmart, Amazon, Costco, TJX) and well‑executing specialty brands (Gap, Ralph Lauren, Tapestry, Levi), a backdrop supportive of margins and full‑price selling into the new year.

Market structure: Holiday data implies winners are omnichannel scale retailers (AMZN, COST, TJX) and digitally native brands that use CRM/AI (KVYO clients, MAT, RL, TPR, LEVI). Lower-than-expected discounting and higher repeat-buyer rates (+25% platform sales, +37% product consideration) increase pricing power and full-price sell-through over the next 1–3 quarters, while big-ticket categories (home improvement) are likely to underperform near-term. Risk assessment: Key tail risks are renewed tariff shocks or CPI re-acceleration that force discounting, and regulatory/data-privacy constraints on conversational AI that would reduce personalization gains; probability medium but impact high. Immediate (days–weeks) sensitivity centers on early results and inventory prints, short-term (weeks–months) on December sales/earnings and 1Q guidance, long-term (quarters+) on AI adoption ROI and margin expansion. Trade implications: Prefer long exposure to CRM/AI enablers (KVYO), scale defensives (COST, AMZN) and select branded apparel/beauty (RL, TPR, LEVI) for 3–12 month horizons; underweight/hedge big-ticket/home-improvement (HD) for the same window. Use options to express convex views (3–6 month calls on KVYO/AMZN; 1–3 month put spreads on HD) and implement pair trades (long COST / short HD) to isolate category rotation. Contrarian angles: Consensus underestimates upside from conservative retailer inventories — if repeat-buyer trends persist, expect a 3–6% revenue tailwind for well-positioned brands into Q1; conversely, AI hype could be overbought in small-cap martech names if privacy regulation tightens. Watch December sales cadence and CPI/ISM prints (next 30–60 days) as catalysts that could quickly re-rate these buckets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment