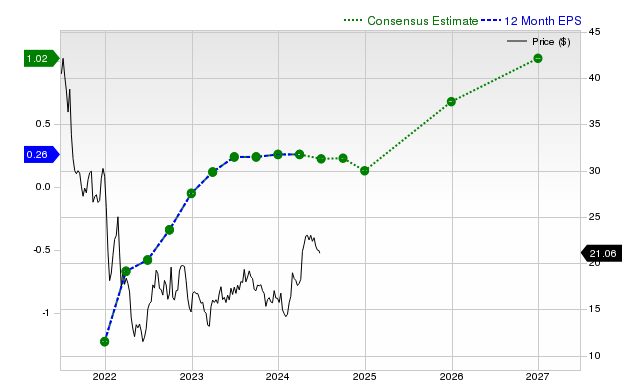

Coupang (CPNG) has garnered significant investor attention despite underperforming the S&P 500 with a 9.6% decline over the past month. While the e-commerce giant projects robust revenue growth, with current quarter sales estimated at $9.15 billion (+16.3% YoY), its earnings outlook is mixed; current quarter EPS consensus estimates have been revised down 23.5% in 30 days, and the last reported quarter saw a 71.43% EPS surprise miss. This combination of strong sales projections and downward earnings revisions has resulted in a Zacks Rank #3 (Hold), indicating an expectation for the stock to perform in line with the broader market in the near term.

Coupang, Inc. (CPNG) presents a conflicting fundamental picture, characterized by robust top-line growth juxtaposed with significant near-term earnings pressure. The company's stock has markedly underperformed, declining 9.6% over the past month against a 2% gain for the S&P 500 composite. Revenue forecasts remain strong, with consensus estimates pointing to 16.3% year-over-year growth for the current quarter to $9.15 billion, and sustained double-digit growth for the current and next fiscal years at 15.5% and 17.8% respectively. This is consistent with its last reported quarter, where revenues grew 16.4% and beat estimates by 1.37%. However, the earnings outlook is deteriorating. The company posted a significant EPS miss of -71.43% in its last report, and analyst consensus estimates for the current quarter and fiscal year have been revised downward by 23.5% and 25.8% respectively over the last 30 days. While the next fiscal year projects a substantial 184.9% EPS increase, the persistent negative revisions and a neutral Zacks Rank #3 (Hold) suggest that translating revenue growth into profitability remains a key challenge and that the stock may perform in line with the market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment