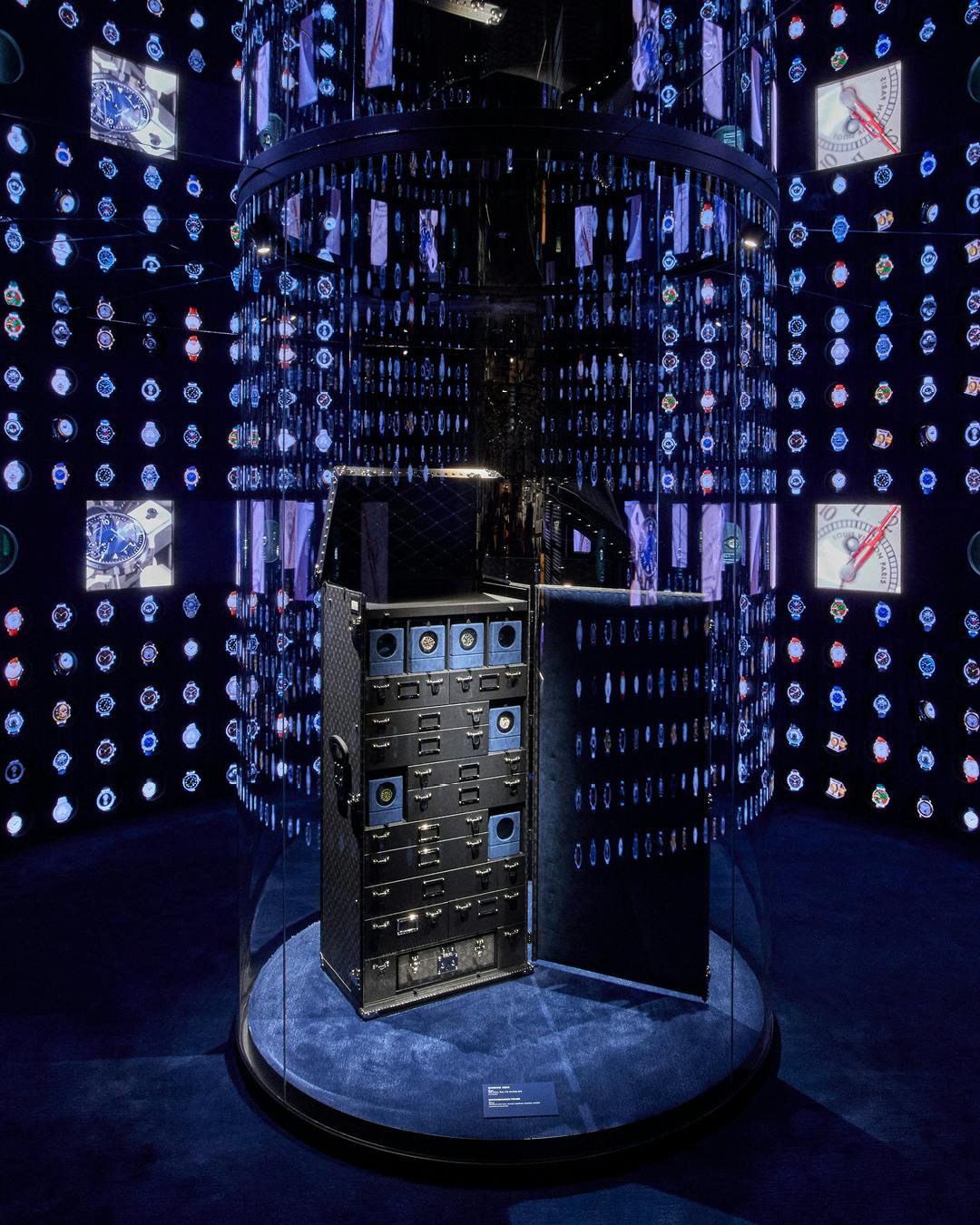

Louis Vuitton opened Louis Vuitton Visionary Journeys Seoul, a six-floor multi-level store and experiential destination inside LV The Place Seoul at Shinsegae The Reserve that combines retail, cultural exhibitions (over 200 pieces) and a gastronomic offering. The venue — conceived with Shohei Shigematsu-OMA and featuring Le Café Louis Vuitton by Maxime Frédéric and a restaurant by two-Michelin-star chef Junghyun Park — extends the Maison’s experiential retail footprint after Shanghai and Bangkok and ties into brand milestones ahead of the Monogram’s 130th anniversary in 2026, reinforcing Louis Vuitton’s strategic engagement with South Korea’s luxury market and customer experience initiatives.

Market structure: Luxury incumbents (LVMH/MC.PA, Hermès/RMS.PA, Kering/KER.PA) and premium Korean retailers (Shinsegae 004170.KS) are the direct beneficiaries — experiential multi-floor flagship stores lift average transaction value (AOV) and frequency versus pure e‑commerce, implying 1–3% incremental Asia revenue potential for a top brand over 12 months and sustained pricing power. Mid‑market and discount apparel retailers are losers as discretionary wallet share shifts to high‑margin experiences; expect high‑end vacancy rates to fall and rents at premium malls to rise, supporting landlord credit in Korea and Paris retail corridors. Risk assessment: Short term (days–weeks) the opening is a media event with minimal P/L; medium term (3–12 months) outcomes hinge on Seoul inbound tourism recovery (threshold: >80% of 2019 arrivals to meaningfully lift footfall) and consumer credit trends in Asia. Tail risks include China anti‑luxury/anti‑extravagance regulatory moves, Korea geopolitical shocks impairing tourism, or execution risk (costly capex diluting margins by >100bp). Hidden dependencies: store sales concentration in a few flagships, local JV/lease terms with Shinsegae, and FX (KRW appreciation versus EUR could lift reported EUR revenues but squeeze local price competitiveness). Trade implications: Direct long: increase LVMH exposure (MC.PA) by 2–3% of equity allocation as a quality cyclical with a 12‑18 month runway to the 2026 Monogram anniversary. Pair trade: long MC.PA vs short KER.PA (equal notional 1–1.5%) to capture execution/omnichannel premium. Options: buy 9–15 month call spreads on MC.PA (+10% / +30% strikes vs spot) to cap risk while leveraging anniversary upside; size ~0.5–1% notional. Contrarian angles: Consensus underestimates the durability of experiential retail — if LVMH demonstrates >2% Asia comp outperformance over two quarters, re-rate compression could be >5% EPS uplift. Conversely, the market may be underpricing a scenario where capex for global rollouts compresses group margins by >50–100bp; watch quarterly gross margin and retail square‑meter productivity for early signs. Historical parallel: Hermès flagship expansion produced multi‑year comp outperformance; failure modes are operational (staffing, supply) not demand.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30