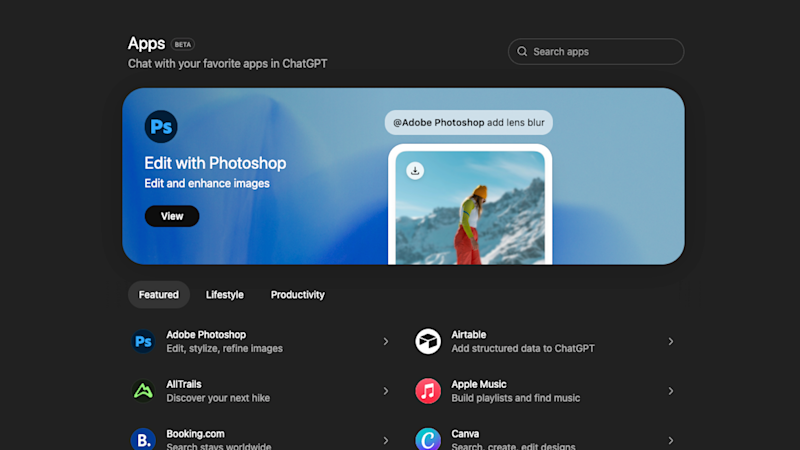

OpenAI has opened third-party app submissions and launched an App Directory accessible in ChatGPT (chatgpt.com/apps), enabling its 800M+ users to discover and use approved third-party apps; submissions went live Dec. 17 and apps that pass review will begin rolling out in early 2026. The Apps SDK supports richer, interactive in-chat experiences, but initial monetization is limited to external purchases of physical goods and all apps must meet OpenAI’s safety, privacy and content guidelines; material questions remain about how OpenAI itself will log or use app interaction data. A developer “Build Hour” is scheduled for Jan. 21 to guide submissions, signaling OpenAI’s strategy to pivot ChatGPT into a distribution platform for AI-native software while keeping review and compliance controls central.

Market structure: OpenAI’s App Directory converts ChatGPT into a distribution layer that disproportionately benefits app‑native software with rich UIs and API hooks (design, education, booking—FIG, COUR, EXPE) by lowering user acquisition costs and accelerating adoption. Network effects and default placement inside 800M+ user sessions increase pricing power for successful apps and give OpenAI latent platform monetization optionality (platform take rates could compress margins for downstream aggregators). Near‑term demand shock will be for developer tools, cloud/GPU capacity and security services; commodities impact (copper/energy) is second‑order and gradual as datacenter buildouts scale over several quarters. Risk assessment: Key tail risks are regulatory privacy enforcement (GDPR‑style fines, forced data residency) and a high‑profile data breach that could freeze app rollouts; both could knock 20–40% off adoption curves for 6–12 months. Timing: immediate (days–weeks) — developer sentiment and sign‑ups from the Jan‑21 Build Hour; short term (3–9 months) — metrics on app approvals and early retention; long term (12–36 months) — monetization and platform fees. Hidden dependencies include OpenAI’s opaque data retention policy, cloud provider GPU availability, and developer economics (ability to monetize outside physical‑goods restriction). Trade implications: Prefer concentrated, option‑light exposure to companies with high UI integration optionality (FIG) and educational commerce (COUR) while hedging regulatory risk. Use LEAP call spreads to express upside (12‑18 month expiries) and buy short‑dated downside protection around regulatory milestones (Jan 21 webinar, early‑2026 rollout). Avoid levered long exposure to pure ad‑driven traffic aggregators until OpenAI’s data‑sharing and retention disclosures are clarified. Contrarian angles: The market underestimates monetization lag — OpenAI bans digital in‑app sales initially, so revenue acceleration will be slower than headlines suggest; price in a 6–12 month realization window. Overreaction risk: if early app metrics disappoint, quality names with product hooks (FIG, COUR) will be oversold — a buying opportunity if developer submissions exceed 1,000 within 90 days or if OpenAI pivots to enabling digital purchases by H1 2026. Unintended consequence: greater centralization of identity/data with OpenAI could spur regulatory fragmentation, raising compliance costs ~5–15% for SMB app builders.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment