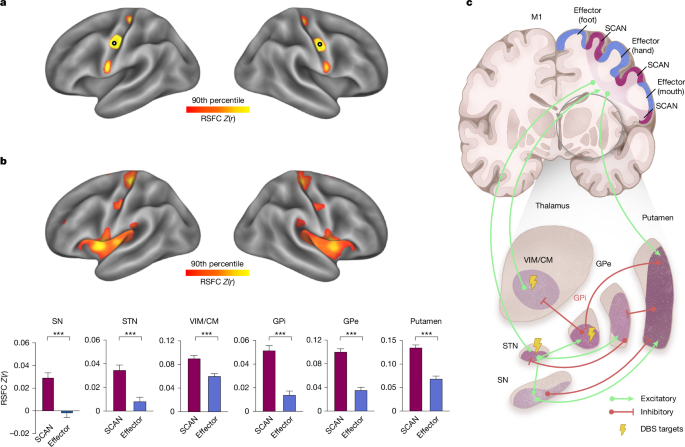

A large multimodal study (n=863 across 11 datasets) identifies a somato-cognitive action network (SCAN) hyperconnectivity signature as central to Parkinson’s disease and shows that established and emerging circuit therapies normalize this signature. Key clinical findings include replication of SCAN hyperconnectivity (PIPD subset n=65 vs 60 controls, t=3.2, P=0.002), longitudinal STN-DBS (n=14) associated with persistent UPDRS-III improvement and attenuation of SCAN-to-subcortex connectivity, personalized rTMS targeting SCAN doubled efficacy versus effector targeting in a randomized 36-patient trial (SCAN group week-2 MDS-UPDRS-III −13.48 vs effector −6.49), and MRgFUS outcomes (n=10) correlated with proximity to a thalamic SCAN hotspot (Spearman ρ = −0.68, P = 0.031). Implication: device makers, neuromodulation vendors and precision-imaging service providers could see incremental opportunity from SCAN-guided targeting and diagnostics, though near-term market impact is moderate given early-stage clinical validation.

Market structure: Precision-SCAN findings create a multi-billion-dollar addressable expansion for device makers (DBS leads, MRgFUS platforms, neuronavigation/imaging) and TMS systems by turning non-invasive treatments into higher-efficacy, repeatable procedures. Near-term winners: large-cap MedTech with DBS franchises (MDT) and imaging/system providers (GEHC) that can bundle MRI + therapy; smaller pure-play TMS names may be optionality plays. Increased demand for MRI time, neuronavigation software and ultrasound systems should lift equipment capex over 6–24 months while supporting modest pricing power for integrated solution providers. Risk assessment: Tail risks include failed multicentre RCTs (low-probability, high-impact within 12 months), adverse reimbursement rulings (CMS/NCD) or patent/IP litigation that could delay adoption 12–36 months. Supply-chain shortages (ASICs, coil components) or rapid competitive commoditization could compress ASPs by ~10–30% over 2–4 years. Key catalysts: FDA labeling, CMS coverage decisions, and large multicentre rTMS/DBS trials expected over the next 6–18 months. Trade implications: Tactical overweight in MDT (market leader in DBS) and GEHC (imaging backbone) is warranted: initiate small positions now and use options to express convexity — buy 9–15 month call spreads to cap premium. BSX is a lower-conviction add (smaller 1–2% position) pending evidence of commercial share gains; avoid small standalone TMS equities until multicentre confirmation. Rotate +3–5% into Healthcare Equipment vs Pharmaceuticals over next 3–12 months; trim defensive bond exposure by 1–2% if equities outperform on catalyst realization. Contrarian angles: Consensus may overstate DBS cannibalization — SCAN-targeted rTMS is likely complementary, expanding the treated population rather than replacing DBS, so device revenue pools could grow not shrink. Market may underprice GEHC exposure to incremental MRI-driven workflow revenue; conversely it may overprice niche TMS pure-plays before reimbursement clarity. Historical parallel: early DBS skepticism followed by durable adoption once trials, reimbursement and surgeon workflows aligned—expect a 12–48 month evidence-to-adoption ramp rather than immediate disruption.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment