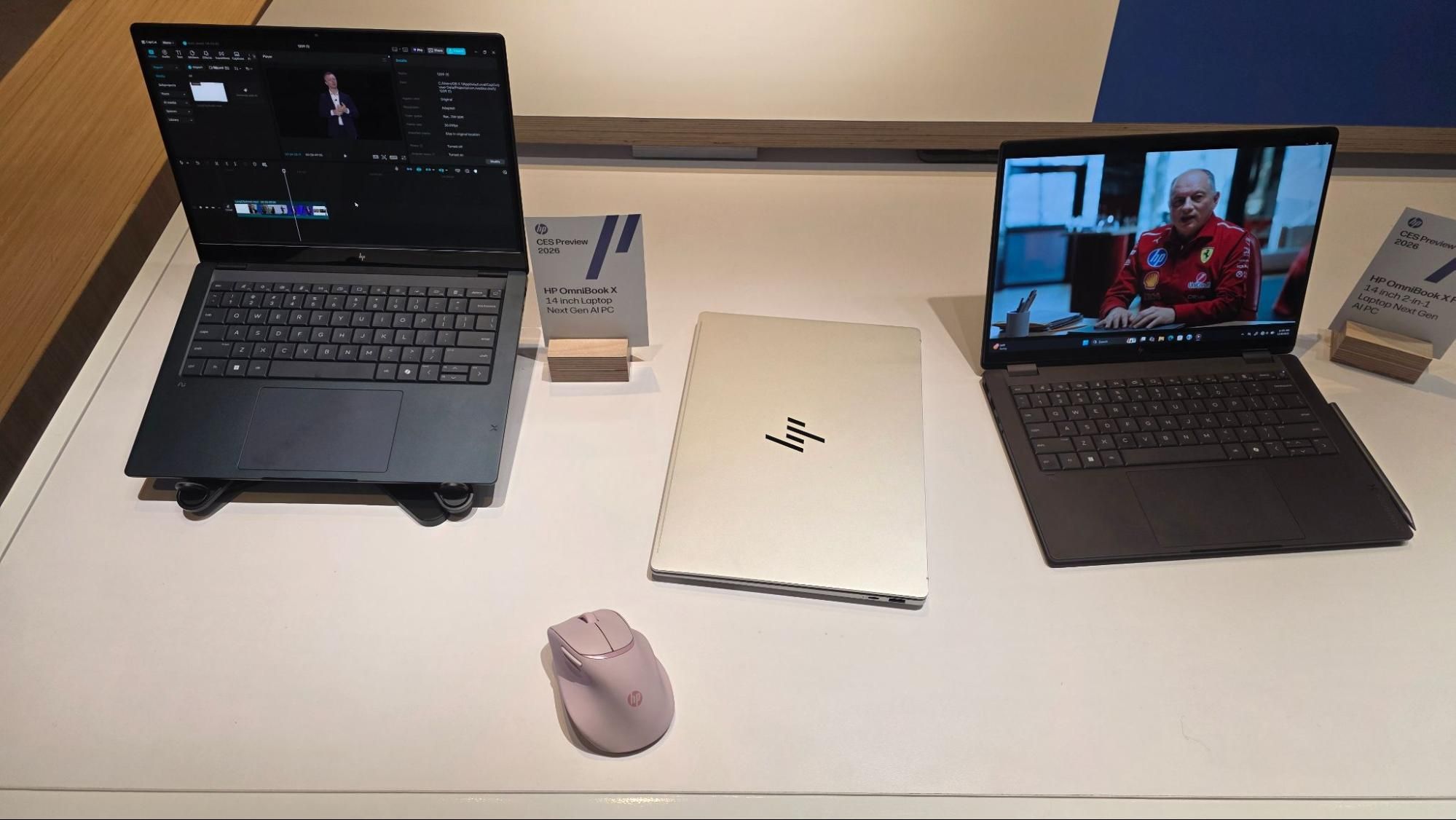

HP refreshed the OmniBook Ultra 14 with new Qualcomm and Intel configurations, highlighting an exclusive Snapdragon X2 Elite variant (X2E-90-100) delivering an 85 TOPS NPU (up from 80 TOPS) and a Qualcomm entry SKU using Snapdragon X2 Plus; Intel models will ship with unspecified Next Gen AI processors (potentially Panther Lake, which would offer up to ~50 TOPS). Both 14-inch OLED 2880x1800 120Hz systems support up to 64GB LPDDR5X (soldered), up to 2TB PCIe Gen5 storage, Wi‑Fi 7, 70 WHr battery, weigh 2.81 lbs and feature similar port layouts; the Intel model is due January 2026 starting at $1,549.99, while the Qualcomm model arrives in spring 2026 with pricing TBD. The upgrades chiefly matter for on-device AI workloads and represent modest competitive product differentiation rather than a material near-term market-moving event.

Market structure: HP (HPQ) and Qualcomm (QCOM) are the direct beneficiaries — HP gains product differentiation and a premium SKU while Qualcomm secures an OEM exclusive X2 variant with 85 TOPS NPU that can command ASP premium and channel priority. Intel (INTC) is at risk of losing feature parity in consumer AI notebooks if Panther Lake NPUs remain ~50 TOPS; that can compress Intel’s OEM pricing power for thin-and-light segments and push buyers toward Qualcomm-equipped SKUs. Supply signs: expect near-term demand pull for high-TOPS SoCs, memory (LPDDR5X) and PCIe Gen5 SSDs; if TSMC capacity is tight, QCOM could see constrained fulfillment that supports prices and short-term equity volatility. Risk assessment: Tail risks include exclusivity reversal, Qualcomm yield problems, or regulatory/antitrust scrutiny of exclusive chip deals — each could drop QCOM/HPQ shares >15% quickly. Time horizons split: Intel SKU launch (Jan 2026) will drive immediate stock moves; Qualcomm model in spring 2026 will be the real adoption test over 3–12 months. Hidden dependencies: on-device AI value depends on software/ecosystem (models, power/thermal limits) — TOPS alone won’t guarantee user adoption; channel inventory dynamics (retail sell-through vs. OEM bookings) are a key second-order risk. Catalysts: independent benchmarks, tear-down supply confirmations, and channel inventory reports will accelerate or reverse trends. Trade implications: Favor semiconductor and OEM exposure to high-TOPS demand: long QCOM (size 2–3% portfolio) and constructive on HPQ (1.5–2%), short small INT C exposure (0.5–1%) or buy 3–6 month put spreads to limit capital. Pair trade: long QCOM / short INTC (2:1 notional) to play product-cycle rotation; trim if QCOM out-performs by >25% or if 60-day sell-through <60%. Options: use defined-risk call verticals on QCOM expiring 6–12 months out to capture adoption while capping premium; consider HPQ March–June 2026 call spread ahead of Qualcomm pricing reveal. Contrarian angles: The market overweights raw TOPS as a proxy for UX — expect diminishing returns once thermal, battery and model-optimization constraints appear, so valuations that price sustained premium revenue growth for QCOM could be premature. Historical parallel: ARM-based laptop early wins (Chromebooks) showed feature wins don’t ensure instant market share — software and enterprise deals matter. Unintended consequence: consumer confusion from mixed Intel/Qualcomm SKUs could prolong substitution, leaving OEM inventory bloated; stop-loss triggers and inventory metrics (sell-through <60% at 60 days) should be hard checks before adding exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment