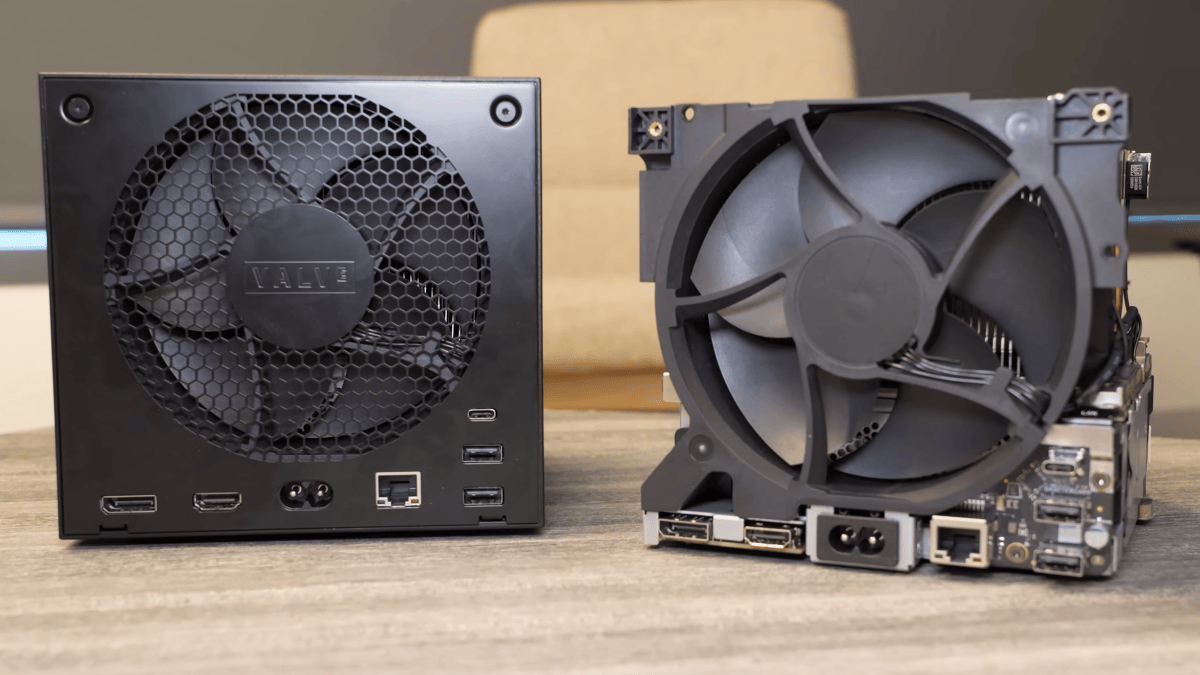

Listings on Czech retailer Smarty.cz — possibly placeholders — show Valve's Steam Machine priced at roughly €988 (512 GB SSD) and €1,111 (2 TB SSD) including 21% VAT, with specs including 16 GB DDR5 and 8 GB GDDR6; the €123 premium between SKUs aligns with current SSD market spreads. Persistent memory shortages driven by AI datacenter demand, which has pushed DRAM and flash prices 2–4x and may persist through 2026, are cited as the likely cause of higher-than-anticipated pricing and pose downside risk to unit demand and launch momentum ahead of Valve's 'early 2026' rollout. Valve has not confirmed pricing and has historically favored direct sales, so margins, channel strategy and consumer uptake remain key uncertainties for financial consideration.

Market structure: The Smarty.cz listing and reported 2–4x spike in DRAM/flash implies Valve’s Steam Machine BOM could be ~€900–1,100, signaling sustained pricing power for DRAM/NAND suppliers (benefit: MU, WDC, Samsung/000660.KS) while compressing margins for compact OEMs and value console competitors. Because Valve won’t subsidize hardware, the unit economics favor component suppliers and Valve’s direct-margin model; consumer adoption may slow if price elasticity exceeds ~20% versus consensus €800, reducing volume vs. expectations. Risk assessment: Tail risks include a sharp memory-price reversal if AI D/C demand normalizes (high-impact, low-probability within 6–12 months), export restrictions on key memory fabs, or Valve changing distribution (operational). Immediate (days) risk is elevated implied volatility; short-term (3–6 months) earnings/capex guidance from MU/WDC are critical; long-term (2026+) the cycle may flip as capex returns create oversupply. Hidden dependency: large long-term contracts by hyperscalers could already lock prices, muting upside for suppliers. Trade implications: Favor cyclical memory longs with volatility-aware sizing: sustained tightness through 2026 should lift supplier revenue 10–30% vs. baseline; pressure on consumer electronics suggests tactical shorts in console/retail names (SONY, HPQ) for 3–6 months. Cross-asset: expect higher equity vol in memory names, modest upward pressure on tech-related inflation, and mild tightening in IG tech capex-linked credit spreads if capex accelerates. Contrarian view: Consensus focuses on higher memory prices as unilateral boon for suppliers but underestimates demand elasticity and potential volume declines that could cap revenue upside; historical 2017–2019 memory boom-bust shows a 12–24 month lead to oversupply. Unintended consequence: elevated component prices may boost the refurbished/used-PC market, capping new-device ASP growth and creating a secondary market arbitrage (buying used GPUs/memory) that erodes OEM margins.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25

Ticker Sentiment