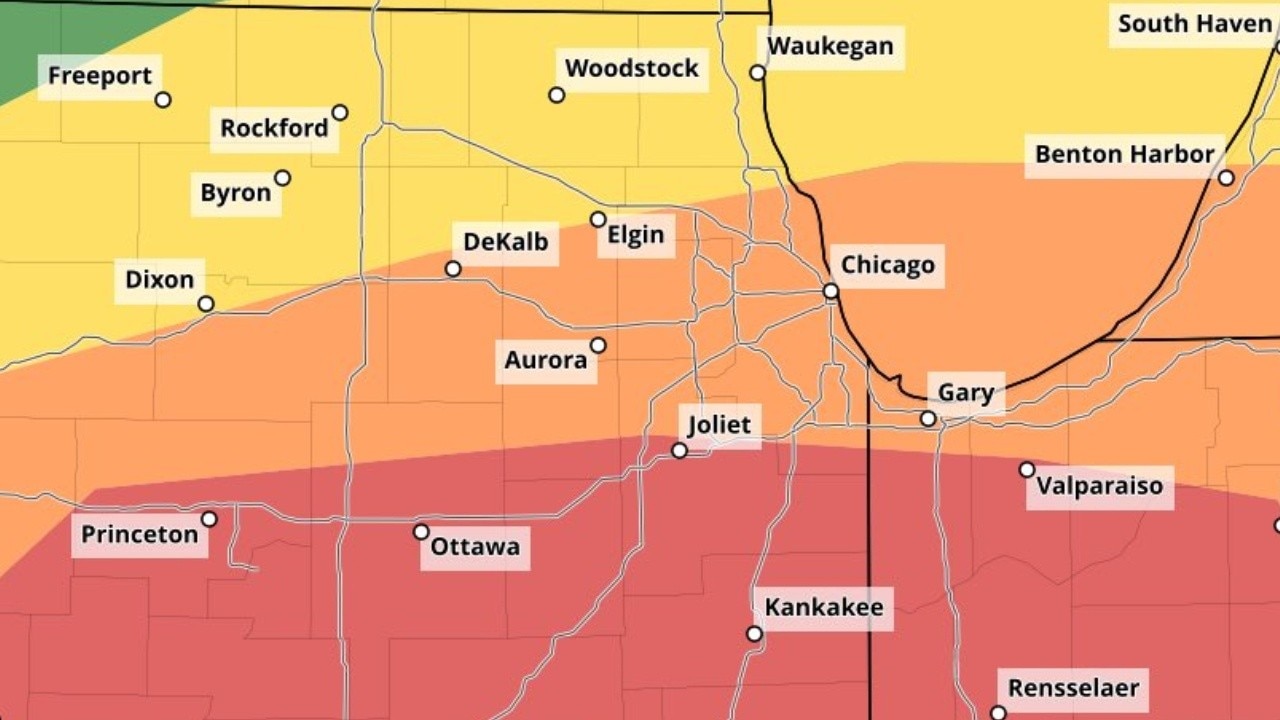

Confirmed large, extremely dangerous tornadoes were reported across NW Indiana and northern Illinois (example: near North Judson moving east at ~20 mph), with the Storm Prediction Center issuing a Moderate Risk (Level 4/5) for southern Chicagoland. Storms are capable of very large hail (>=2 in), wind gusts >70 mph and tornado probabilities of 15–29% south of I‑80 in a threat window roughly 3 p.m. Tuesday–1 a.m. Wednesday. Operational impacts include ground stops at Midway (until ~9:00 p.m.) and O'Hare (until ~8:30 p.m.), road closures (e.g., Route 45/52 near I‑57), and extensive damage reported in Kankakee/Aroma Park with emergency services overwhelmed.

This kind of concentrated severe-weather outbreak creates predictable, short-duration economic shocks with patchy spatial footprints: immediate operational hits to hub airports and regional trucking routes, followed by a 4–12 week ramp in demand for vehicle glass/auto-body parts, roofing materials, and temporary power services. Expect aftermarket parts suppliers and home-improvement retailers to see an identifiable revenue uptick concentrated in the Midwest; that demand is typically high margin and converts to cash quickly, so equities with clean inventories can see outsized upside within 2–8 weeks.

Insurance and reinsurance are the obvious headline losers, but losses will mostly migrate into loss-adjustment and reinsurance layers — large national reinsurers absorb the tail, while primary personal-auto and homeowner writers see immediate hit to combined ratios. Market pricing tends to overshoot on day-one: a medium-sized outbreak can pressure an auto insurer’s quarterly loss ratio by a few percentage points (single-digit EPS drag) but rarely forces balance-sheet impairments unless multiple events stack.

Logistics and e-commerce firms face two distinct frictions: (1) hub congestion creates short-term multi-day shipping delays that temporarily depress fulfillment metrics and raise expedited-shipping costs; (2) localized road/bridge damage increases trucking cycle times in affected counties for weeks. These second-order costs are usually transitory but concentrated enough to create asymmetric opportunities for contractors and parts suppliers.

Contrarian lens: the market’s knee-jerk negative read on insurers and airlines often overprices one-night operational disruption and underprices the follow-on revenue bump to building-materials and aftermarket parts. If claims severity remains within modeled catastrophe-exposure bands, select repair-oriented names re-rate quickly while select insurers recover after reserve adjustments are communicated over subsequent reports.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60