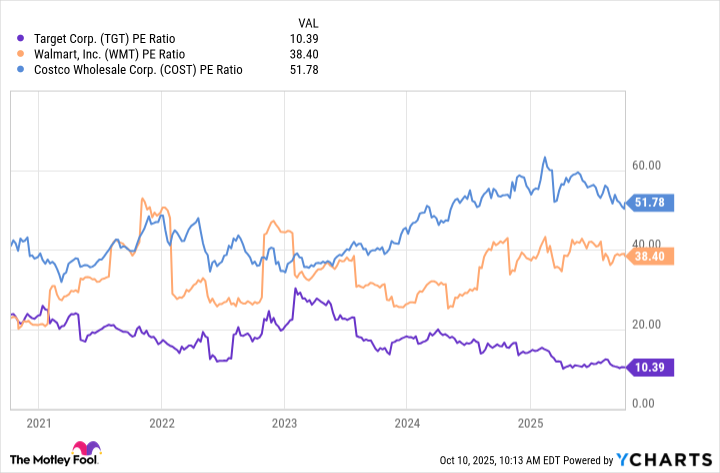

Target (TGT), a Dividend King with 54 consecutive payout hikes and a current 5% yield, is highlighted as a compelling value despite recent sales declines and a CEO change. The company's dividend remains well-covered by its free cash flow, and strategic investments of $4-5 billion over five years are planned to drive $15 billion in new sales, with analysts forecasting a 2% sales increase next fiscal year. Its current P/E ratio of 10 suggests the stock is oversold, indicating potential for significant multiple expansion and outsized returns if its turnaround efforts succeed.

Target (TGT), a Dividend King, offers a 5% dividend yield, significantly above the S&P 500 average, supported by its 54th consecutive annual payout hike. Despite recent business challenges, including a 2% net sales decline and 3% comparable sales drop in H1 FY25, its $2.94 billion in free cash flow over the last twelve months comfortably covers the $2.05 billion in dividends paid. The company faces headwinds from falling sales and a recent CEO change, contrasting with competitors like Walmart and Costco, which reported robust sales growth. However, Target plans significant strategic investments of $4-5 billion over the next five years in stores, technology, and supply chain, aiming to generate an additional $15 billion in sales. Analysts forecast a 2% net sales increase for the next fiscal year, signaling potential stabilization. Target's stock appears oversold, trading at a P/E ratio of 10, considerably lower than its peers. This valuation, combined with its strong brand recognition and extensive U.S. footprint, presents a compelling value proposition. A successful execution of its turnaround strategy could lead to significant multiple expansion and outsized returns for investors, alongside continued dividend growth.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.60

Ticker Sentiment