Long-end interest rates are rising, particularly in Japanese Government Bonds (JGBs), driven by changes in Japanese economic fundamentals, including nominal income and wage growth. The Bank of Japan (BOJ) has responded by adjusting its yield curve control and raising short-term interest rates, aiming to normalize yields after decades of slower growth. Meanwhile, in the U.S., a proposed budget plan featuring spending cuts and tariffs is expected to be contractionary, yet concerns about the deficit impact may be overblown relative to the "current law" baseline.

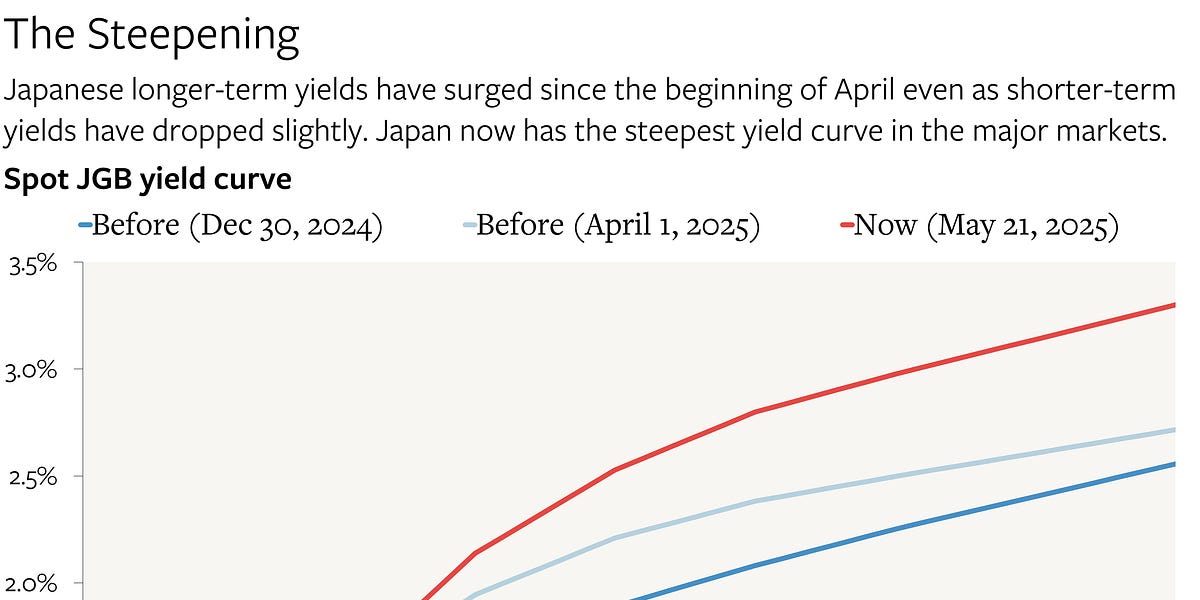

Global long-end interest rates are undergoing a period of normalization, driven by shifts in economic fundamentals, most notably observed in the Japanese Government Bond (JGB) market. Ultra-long-term JGB yields have risen sharply, with 30-year JGBs hedged into U.S. dollars yielding approximately 7%, reflecting a significant repricing from previously suppressed levels. This market adjustment, while causing a collapse in perceived JGB market functioning as of early May, is largely attributable to Japan's improved economic performance post-pandemic. Japanese nominal GDP grew by an average of 4.4% annually from Q4 2022 through Q1 2025, and 5% over the past four quarters, a stark contrast to the 0.2% average annual growth in 2016-2019. Concurrently, Japanese consumer prices are rising around 3.5% (April 2025), with underlying inflation stabilizing near 1.5-2%, and negotiated wages have increased over 5% for two consecutive years, the highest since 1991. Consequently, the Bank of Japan (BOJ) has begun to normalize policy, lifting its 10-year JGB yield cap, reducing asset purchases, and raising short-term rates since March 2024, acknowledging the risks and volatility inherent in this transition; for instance, a 40-year JGB purchased in April 2024 at a 2% yield now faces an unrealized loss exceeding 30%. In the U.S., a proposed budget featuring spending cuts on social programs and green energy subsidies, alongside tariffs, is anticipated to be contractionary. Critically, the projected $3.1 trillion incremental debt increase over ten years from this budget, according to the CRFB, is substantially less than prior estimates based on campaign promises and may result in minimal net debt increase versus the 'current law' baseline if tariff revenues are factored in, challenging narratives that attribute rising U.S. bond yields solely to fiscal profligacy.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

Positive

Sentiment Score

0.30