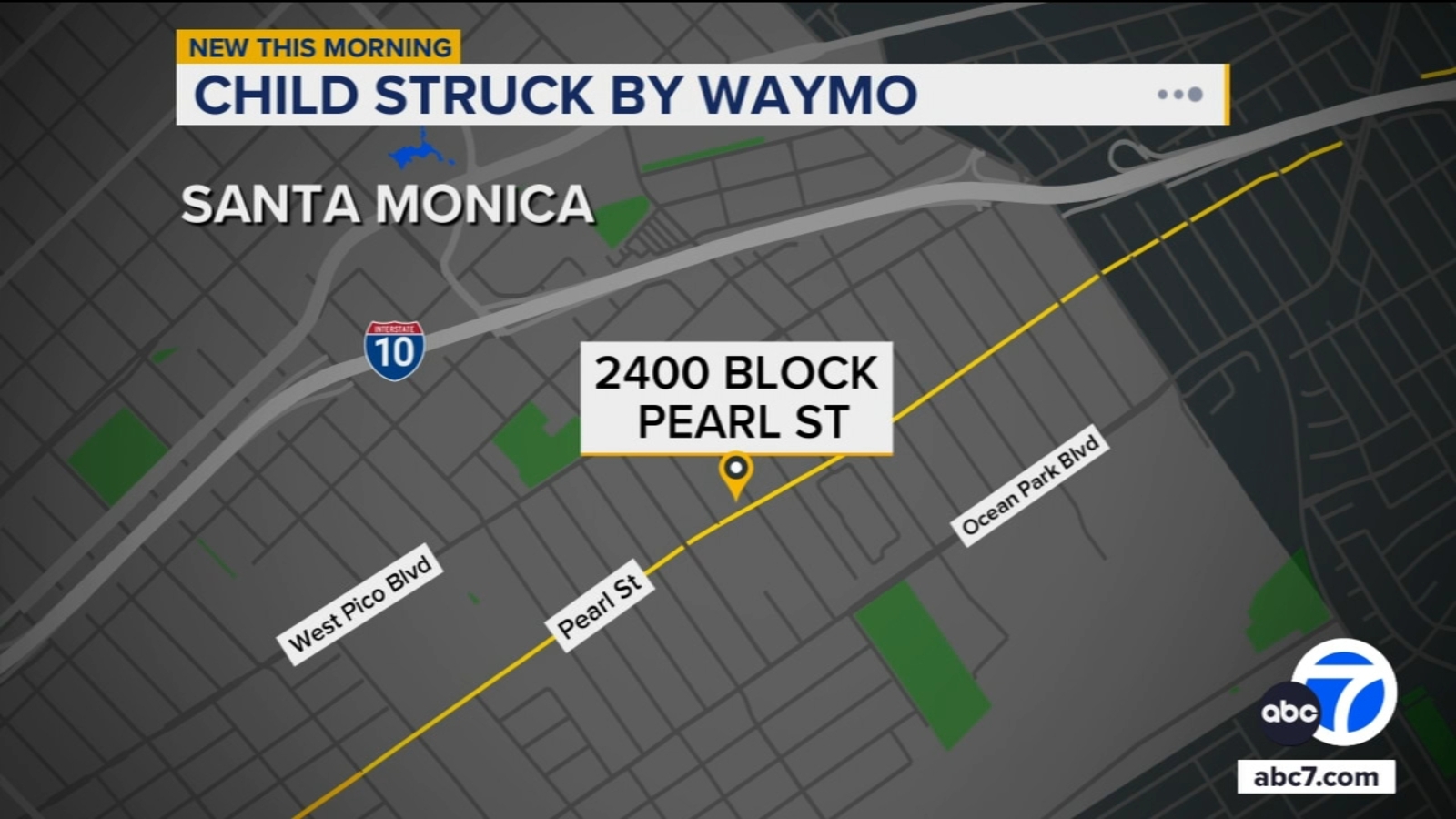

A Waymo autonomous vehicle struck a child near Grant Elementary School in Santa Monica on Jan. 23 after the child entered the roadway from behind an SUV; the child sustained minor injuries. Waymo reported the car braked from 17 mph to 6 mph and voluntarily contacted the National Highway Traffic Safety Administration, which has opened an investigation. The incident raises regulatory and safety scrutiny risks for Waymo and the autonomous-vehicle sector, potentially affecting near-term public perception and regulatory interactions though immediate financial impact appears limited.

Market structure: This incident favors deep-pocket incumbents (Alphabet/GOOGL, NVDA) and established Tier-1 suppliers (APTV) who can absorb regulatory compliance costs, while hurting small pure-play AV firms and lidar specialists (LAZR) through reputational and deployment slowdowns. Expect near-term redeployment of capital toward safety/ADAS retrofit suppliers and insurers that can reprice risk; robo-taxi miles in affected cities could drop 10–30% over the next 1–6 months under heightened scrutiny. Cross-asset: small-cap AV equities implied vol could spike 30–70%, equity flows into defensive autos/insurers, minor downward pressure on municipal yields in affected jurisdictions, FX impact negligible. Risk assessment: Tail risks include a federal operational pause or new binding regs (weeks–3 quarters) that could produce >50% revenue decline for startups and force contract cancellations; for Alphabet the P&L hit is likely <1% of revenue but reputational/pricing multipliers matter. Hidden dependencies: insurer litigation, OEM indemnity clauses, and data-logging rules could shift costs to suppliers; a negative NHTSA finding within 30–90 days is the key catalyst. Monitor state AG actions and NHTSA preliminary reports as 0–90 day triggers. Trade implications: Tactical: overweight GOOGL by 1–2% vs. S&P over 3–6 months (buy-dated 3M), buy APTV 1–1.5% for exposure to safety hardware, and establish a 0.5–1% short or buy 3M put-spread on LAZR (e.g., 15%–25% OTM) to capture outsized vol and deployment risk. Pair trade: long APTV + short LAZR (size 1:1) for 3–6 months. Options: purchase LAZR 3M 20% OTM puts or sell short-dated calls on small AV ETFs; take profits or cut losses at ±25%. Contrarian angles: Consensus will over-penalize major tech parents; past autonomous-vehicle incidents (Uber 2018) produced temporary drawdowns that normalized within 6–12 months while large-cap AI/chip winners accelerated. If NHTSA outcomes are merely procedural (not prescriptive bans) expect a relief rally—consider buying GOOGL/ NVDA call spreads 3–6 months out if NHTSA report is benign. Conversely, overregulation is the underrated risk that could structurally slow TSLA’s robo-taxi timeline and advantage incumbents with regulatory expertise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25