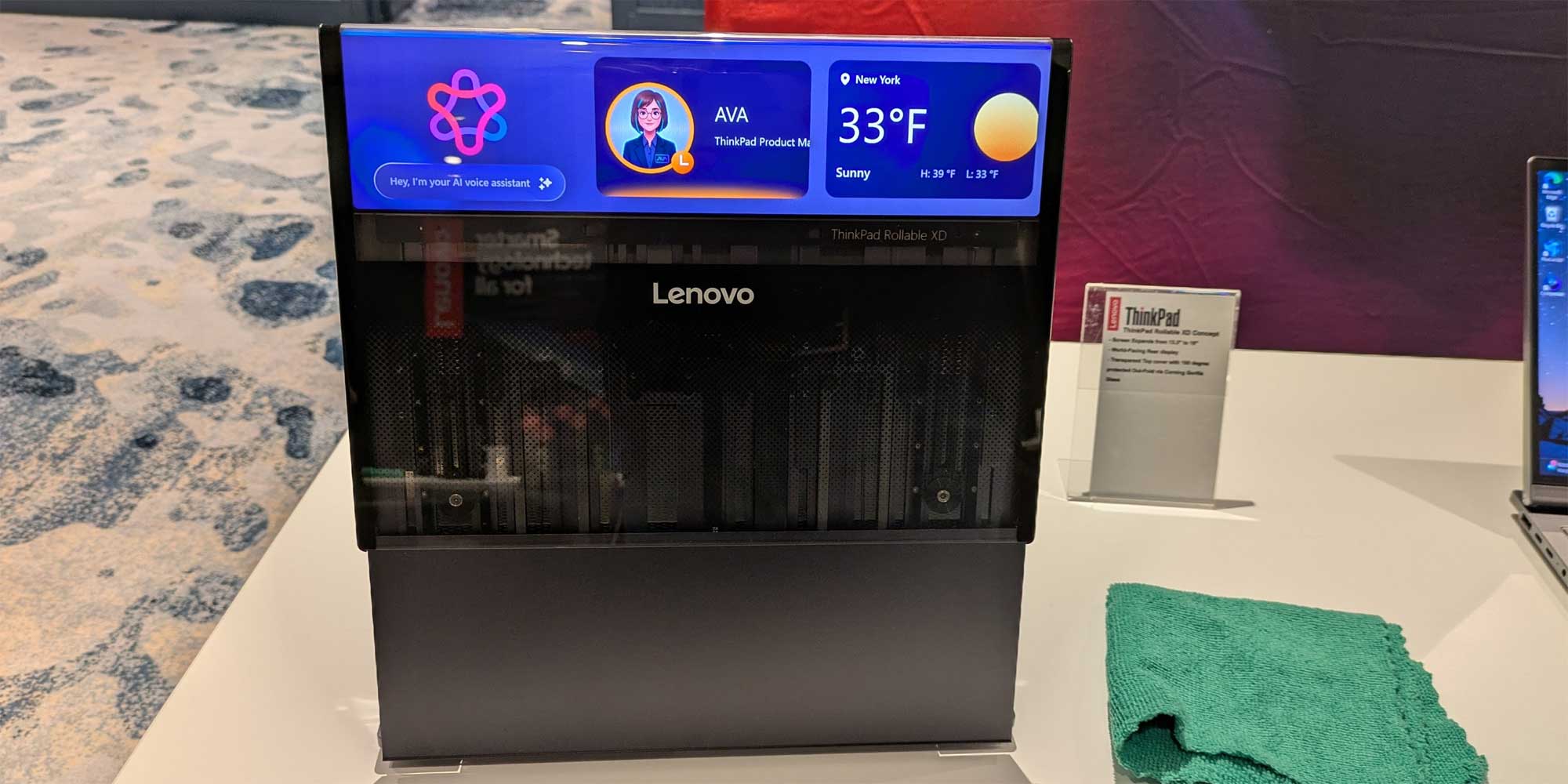

Lenovo debuted multiple novel laptop designs including the ThinkPad Rollable XD and Legion Pro Rollable concepts (expandable OLED displays and gaming-focused AI features), and a motorized convertible ThinkBook Plus Gen 7 Auto Twist powered by Intel Core Ultra Series 3; the Auto Twist starts at $1,649 in the US and ships in June. The company also refreshed the ThinkPad X1 Carbon (Gen 14) with a 'Space Frame' internal layout to improve repairability and cooling, enabling sustained 30W CPU operation; the X1 Carbon Gen 14 and X1 2-in-1 Gen 11 start at $1,999 and $2,149 respectively and go on sale in March. While the rollable designs remain concepts with uncertain commercial timing, the product updates and highlighted use of Intel’s latest chips and AI features represent potential incremental demand and differentiation in Lenovo’s premium PC lineup.

Market structure: Lenovo’s rollable and motorized designs primarily benefit Intel (IN T C) and Nvidia (NVDA) indirectly via higher-spec CPU/NPUs and GPUs in premium SKUs, and Microsoft (MSFT) through Copilot+ OEM tie‑ins that raise ASPs by an estimated $100–200 per unit if adopted. AMD (AMD) faces modest share pressure in enterprise/pro-sumer Lenovo models where Intel’s 18A Core Ultra is highlighted; OEMs like DELL/HPQ may need to match features or concede pricing. Supply signals point to constrained flexible OLED and motorized hinge components — expect component suppliers to gain bargaining power, tightening supply and lifting input prices near term. Risk assessment: Tail risks include display yield failures, patent litigation on mechanical displays, and renewed US-China chip export controls that could cut Lenovo’s supply or Intel’s foundry access; any of these could wipe >10–20% off expected unit economics. Time horizons: immediate price impact is small (days), product availability catalyzes revenue in 1–3 months (Auto Twist in June, X1 in March) and adoption / share shifts play out over 12–24 months. Hidden dependencies: ecosystem success relies on display vendors (Samsung/BOE), Intel 18A capacity, and Microsoft OEM software deals; watch inventory and channel sell‑through next two quarters. Trade implications: Tactical trades include a modest long on INTC (2–3% portfolio) via 12–18 month calls to capture mobile CPU wins, paired with a smaller short in AMD (1–1.5%) to hedge alt architectures. Play NVDA with a 1–3 month call‑spread into gaming/RTX cycle (buy ATM call, sell 10–15% OTM) to limit IV risk ahead of channel announcements. Rotate: overweight semiconductors and enterprise SW (MSFT +2%) and underweight consumer OEMs DELL/HPQ (-2 to -4%) until proof of consistent ASP lift or volume scale. Contrarian angles: The market may be over‑enthusiastic about immediate revenue — these are largely concepts and mechanical complexity historically delays scale (see early foldable phones, multi‑year adoption). If adoption stalls, OEMs will face higher warranty/repair costs and secondary market cannibalization that could compress margins by 200–300bps. A conservative trigger: if Lenovo (or peers) fail to convert >10% of demo interest into unit shipments within 6–12 months, reprice semis exposure downward aggressively.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment