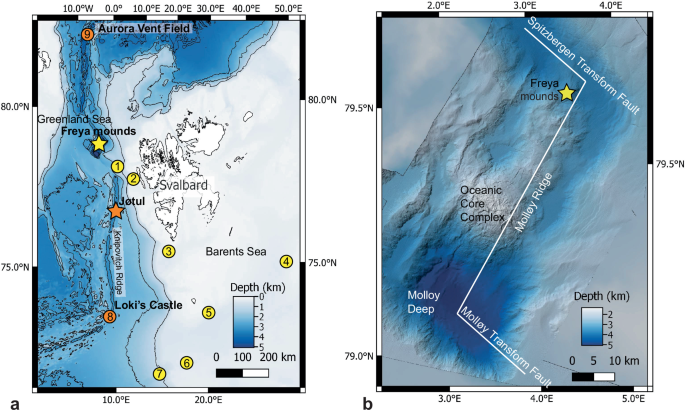

A research team discovered thermogenic gas hydrate mounds at 3,640 m on the Molloy Ridge containing methane-rich gas (C1 ≈ 66%, C2 ≈ 8%, C3 ≈ 14%, C1/(C2+C3) ≈ 3.0) with isotopes δ13C ≈ −47‰ and δD ≈ −188.5‰ and oil signatures pointing to a young Miocene fresh‑brackish source. Gas flares from the site rise to within ~300 m of the surface and a modeled hydrate stability zone is ≈248 m thick, implying meaningful in-situ hydrocarbon potential while also creating ESG and regulatory exposure as Norway moves to manage deep‑sea mining and habitat protection in the region.

Market structure: This discovery is a clear signal to specialized subsea-technology and environmental-monitoring suppliers (ROV operators, geophysical surveyors, analytical labs) as near-term winners because activity (surveys, sampling, monitoring) will accelerate; expect 5–15% incremental project spend regionally over 12–24 months. Pure-play deep‑sea miners and small explorers face reputational and regulatory downside as Arctic protection debates intensify, increasing financing costs and delaying projects. Commodity supply impact is negligible in the next 3–5 years — commercial hydrate production remains technically speculative — but a credible long-term (5–15y) new gas source would cap LNG price upside if extraction pathways emerge. Risk assessment: Tail risks include: (A) swift regulatory moratoriums in Norway/EEZ or by ISA that can wipe 30–70% of junior miner valuations within weeks; (B) a large methane release prompting carbon/regulatory shocks and insurance repricing. Immediate window (days): low market movement; short-term (weeks–months): policy headlines and NGO campaigns will drive volatility; long-term (years): technology viability and climate policy determine value. Hidden dependencies: insurance, bank financing and ESG mandates are binary gatekeepers for project viability and can change valuations faster than technical progress. Trade implications: Tactical plays favor suppliers and analytics over miners. Consider small, time-bound longs in established subsea/ROV and analytical equipment providers (12–24 month horizon) and defensive longs in diversified energy majors to hedge commodity sentiment. Use option structures to express asymmetric views: buy long-dated puts on speculative miners and sell covered calls or buy calls on subsea services if regulatory risk eases. Contrarian angles: Consensus overstates immediate resource value and understates regulatory inertia — commercial extraction is unlikely before ~2030 absent major tech breakthroughs. That suggests current enthusiasm in junior miners is potentially overdone; a measured short/put exposure to these names vs. a long in environmental analytics/monitoring is a high-information trade. Watch for the next 60–180 day regulatory decisions (Norwegian EEA, ISA) as catalysts that will reprice this sector.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment