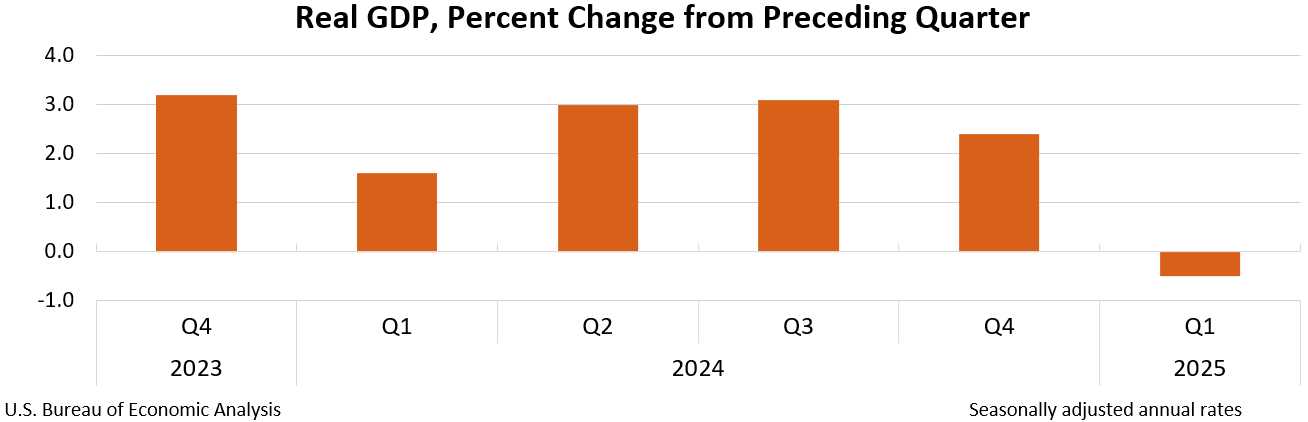

The U.S. economy contracted in the first quarter of 2025, with real GDP decreasing at an annual rate of 0.5 percent, a downward revision from earlier estimates and a significant slowdown from Q4 2024's 2.4 percent growth. This deceleration was primarily attributed to increased imports and decreased government spending, despite some offsetting increases in investment and consumer spending, the latter of which saw substantial downward revisions. Concurrently, corporate profits decreased by $90.6 billion, while key inflation measures, including the PCE price index, rose by 3.7 percent, indicating persistent price pressures amidst economic cooling.

The third estimate for Q1 2025 confirms a contraction in the U.S. economy, with real GDP revised downward to a 0.5% annual decrease, a significant reversal from the 2.4% expansion in Q4 2024. The downturn was primarily driven by an increase in imports and a decrease in government spending. More concerning is the signal of weakening domestic demand, as real final sales to private domestic purchasers, a key underlying metric, rose just 1.9%, a substantial 0.6 percentage point downward revision from the prior estimate. This revision was led by weaker consumer spending on services. Compounding the growth concerns, inflationary pressures remain persistent and slightly higher than previously thought, with the PCE price index revised up to 3.7% and the core PCE index to 3.5%. This stagflationary dynamic of negative growth and elevated inflation is further evidenced by a $90.6 billion decline in corporate profits. A slight mitigating factor is the conflicting signal from Real Gross Domestic Income (GDI), which rose 0.2%, suggesting the economic weakness may be less severe than the headline GDP figure indicates.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60