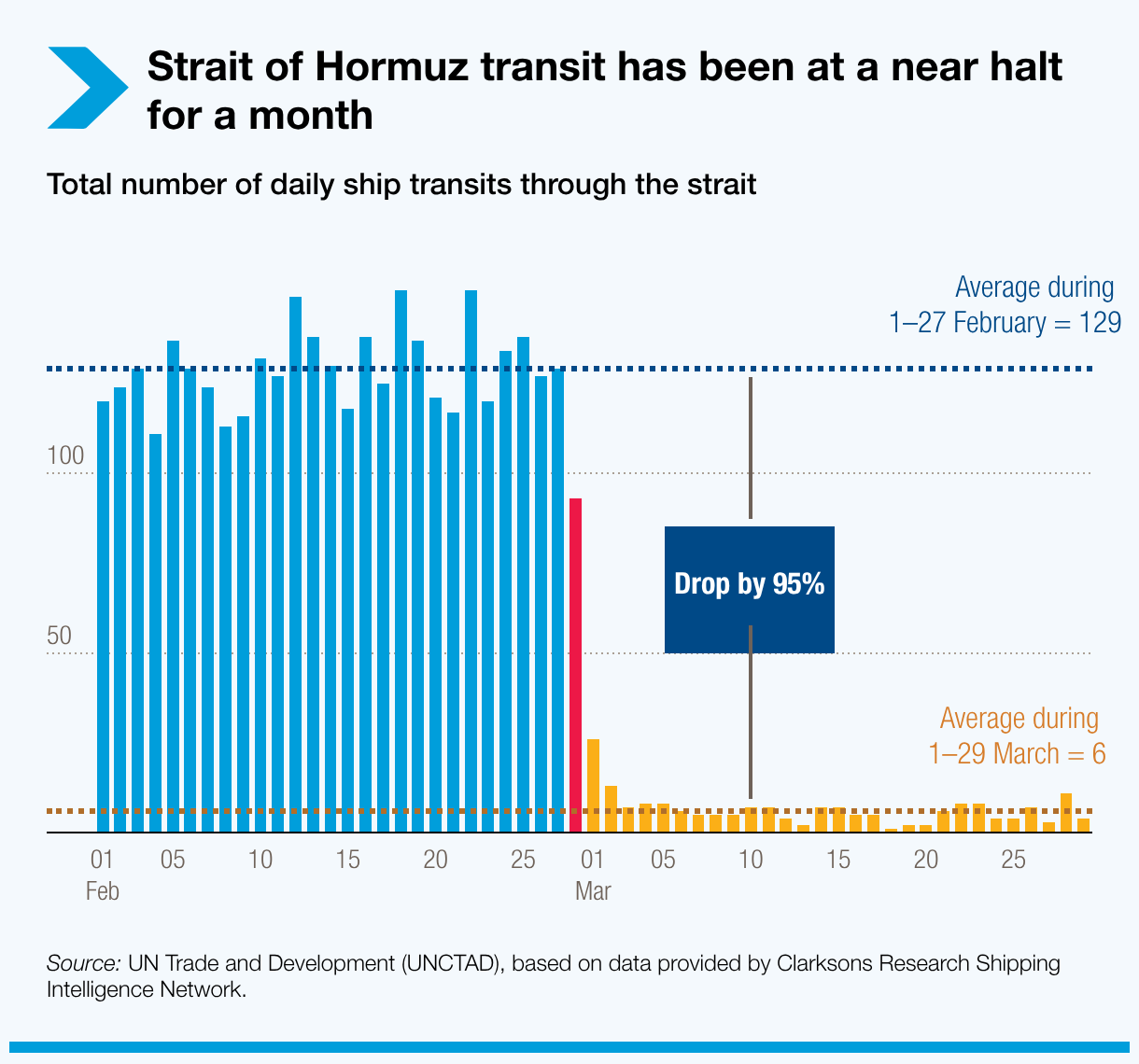

Ship transits through the Strait of Hormuz plunged ~95% (from ~130/day to 6/day), effectively halting a key energy corridor and sharply lifting fuel and shipping costs. UNCTAD now expects global merchandise trade growth to slow from ~4.7% in 2025 to 1.5–2.5% in 2026 and global GDP to ease from 2.9% to 2.6% in 2026, while inflationary pressures and transport costs rise. Financial conditions are tightening in developing markets—currencies weakening and borrowing costs up—as investors pull back, and 3.4 billion people live in countries already spending more on debt servicing than on health or education, heightening sovereign debt and food-security risks.

A chokepoint in Gulf waters acts like a sudden step-change to variable shipping costs and risk premia: insurers reprice war/expropriation exposure, which forces shippers to either reroute (adding voyage days and fuel burn) or demand higher freight rates. The immediate mechanistic effect is a steepening of delivered-cost curves (FOB → CIF), compressing margins for downstream manufacturers and import-dependent governments while boosting bargaining power for sellers with flexible export routes or floating storage. Second-order winners are assets that capture optionality in physical gas/oil logistics — floating storage, regas terminals and fast-cycle producers who can redirect cargoes and raise spot volumes. Losers are balance-sheet constrained importers and any corporate with tight working-capital needs exposed to FX pass-through (airlines, low-margin container operators, fertilizer importers). Expect persistent cross-asset correlations to change: EM sovereign spreads, freight derivatives and commodity vol will move together, making traditional equity-bond hedges less effective. Key catalysts and time horizons: insurance normalization or a diplomatic corridor can unwind most dislocations within weeks if shipping resumes; damage to terminals or sustained embargoes would push effects into quarters and force permanent rerouting and capex to alternative corridors. Central bank responses matter — if core inflation re-accelerates, policy tightening will amplify financial stress in vulnerable sovereigns, raising default risk over 6–24 months. Capital allocation should prioritize convex, optionality-rich exposure and explicit hedges against FX/sovereign stress. Use small, liquid positions to express directional views and buy insurance (FX puts, CDS, commodity call spreads) rather than one-way beta until volatility and insurability normalize; calibrate sizes to sovereign- and counterparty-specific failure modes rather than index-level VaR alone.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75