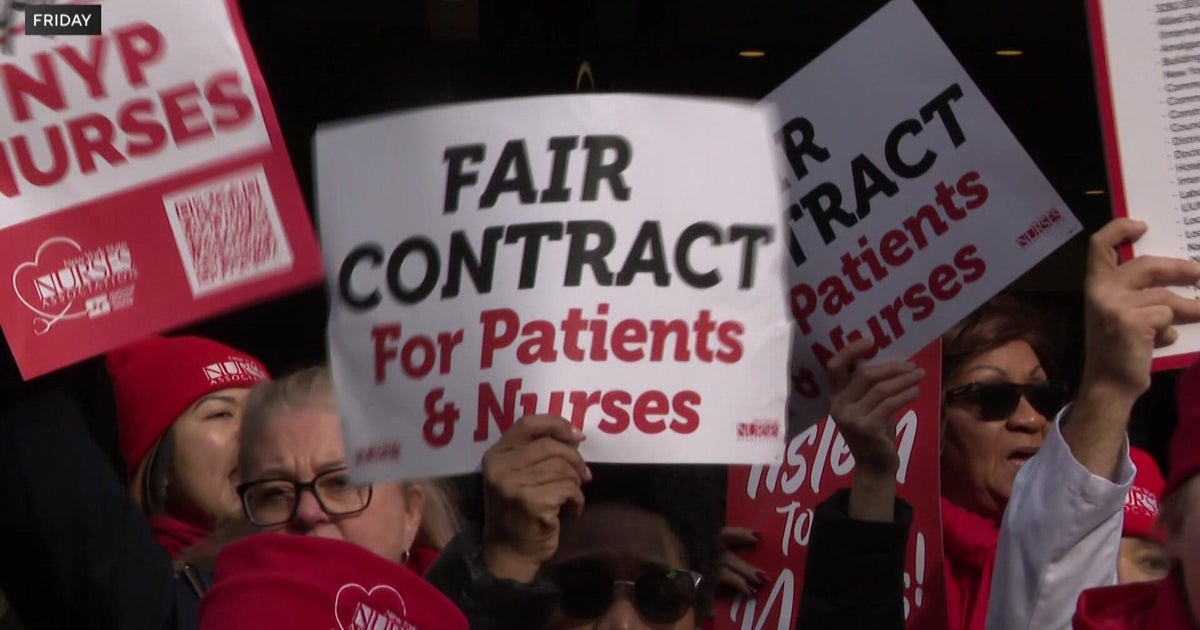

Nearly 15,000 nurses began the largest strike in New York City history at five privately‑run hospitals — Mount Sinai Hospital, Mount Sinai Morningside, Mount Sinai West, Montefiore Einstein and NewYork‑Presbyterian — after contract talks with the New York State Nurses Association collapsed over pay, staffing levels, benefits, pensions and workplace protections. Governor Kathy Hochul declared a state of emergency and ordered state health staff to the impacted hospitals while systems say hospitals will remain open; both sides warned of patient-care and operational risks. For investors, immediate market impact should be limited given many systems' non‑public status and contingency plans, but a prolonged work stoppage could raise near‑term staffing costs, disrupt service volumes and create reputational risk for the affected health systems.

Market structure: Immediate winners are staffing and travel-nurse providers (e.g., AMN, CCRN) and temporary labor brokers as hospitals source contingents; direct losers are the struck NYC systems (non-public) and labor-intensive operators nationwide facing upward wage pressure (likely +5–15% across nurses if precedent sets). Pricing power shifts toward labor and staffing vendors; hospitals may push costs to payors over 6–12 months, pressuring margins by an estimated 1–3 percentage points EBITDA for exposed operators. Risk assessment: Tail risks include a prolonged strike (>4 weeks) that forces revenue loss >5% for impacted facilities, state fines, or emergency regulatory actions that could widen credit spreads 100–300bp for local hospital debt; contagion to other metro systems would materialize over 1–3 months. Hidden dependencies: travel-nurse supply constraints, Medicare/Medicaid reimbursement lag, and union settlements that become national benchmarks. Key catalysts: NYSNA settlement (expect decision within 7–21 days) and any state-mandated staffing ratios. Trade implications: Tactical trades: long staffing agencies (AMN, CCRN) and buy short-dated call spreads (3 months) given near-term demand spike; hedge or short operationally-levered hospital operators (HCA, UHS) via 3–6 month put spreads to cap cost. Credit trades: opportunistic buys of affected hospital revenue bonds if spreads widen >100bp vs MMD; pair trade long AMN, short HCA (relative-exposure hedge) for 3–6 months. Contrarian angles: Consensus may overstate permanent revenue loss—hospitals remain open and state staff deployed, so market overreaction on public names could be short-lived (resolution commonly within 1–3 weeks historically). Conversely, if settlements include guaranteed staffing ratios or >8% wage increases, the structural margin shock is underpriced. Unintended consequence: sustained higher labor costs accelerate automation/telehealth adoption—look for beneficiaries (software, telehealth vendors) over 6–18 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35