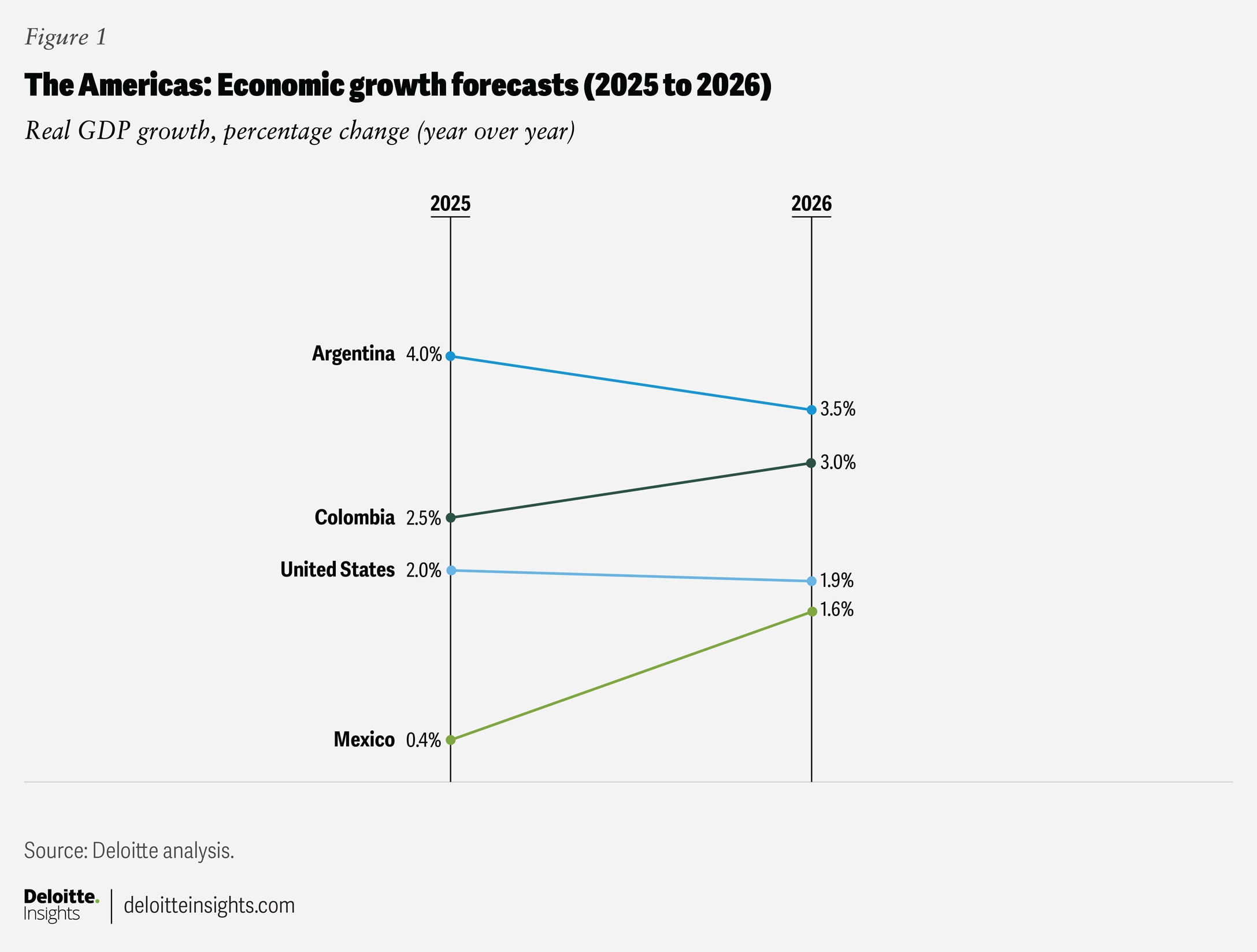

Restrictive U.S. trade measures in 2025—followed by selective trade deals—have disrupted supply chains, raised costs, and reshaped capital flows, with ripple effects expected to dominate 2026. Key country takeaways: Argentina’s stabilization program cut inflation from near 300% in 2024 to projected 29.4% in 2025 and 13.7% in 2026 while GDP rebounds (4.0% in 2025, 3.5% in 2026) and external surpluses return; the U.S. is resilient with ~2% growth in 2025 and AI-driven business investment underpinning activity; China is set to moderate to ~4.5% in 2026; India remains the standout with ~7.5%–7.8% FY25/26 growth. Central banks and fiscal authorities are largely cautious—some easing where inflation allows—while tariffs, geopolitics and FX movements remain the principal market risks for exporters and fixed-income spreads.

Market structure: The big winners are resource exporters and nearshoring hubs — Argentina (energy/lithium/copper via RIGI), Mexico (manufacturing), and targeted miners (lithium/copper/oil & gas). Losers are export-dependent manufacturing in tariff-exposed Europe and US-importers facing higher input costs; expect margin pressure and slower capex in affected sectors. Cross-asset: anticipate wider EM FX dispersion, commodity upside for energy and battery metals, and higher idiosyncratic sovereign spread volatility (Argentina CDS fell from ~2,500bp to ~600bp; further compression possible with IMF disbursements). Risk assessment: Tail risks include tariff escalation (15%+ reciprocal moves), a sharp AI-equity unwind that curtails US consumption, or reversal of Argentina reforms; each could trigger 10–30% moves in equities/FX within weeks. Time horizons: immediate (days–weeks) = FX and commodity volatility; short (3–6 months) = reallocation to Mexico/mining as projects ramp; long (12–36 months) = structural reorientation of supply chains. Hidden dependency: Argentina’s gains hinge on full capital-account liberalization and IMF tranches; delays spike funding risk. Trade implications: Tactical long-in-EM resource/nearshoring exposure, hedged by short EU export names. Use concentrated option structures to express commodity upside while capping downside (6–12 month call spreads on lithium miners, short-dated puts on AI leaders). Fixed-income: favor selective EMBs with improving fiscal trajectories (Mexico, Ghana) and avoid long-duration exposure in tariff-hit economies. Contrarian angles: Consensus underprices Argentina’s resource-driven current-account swing — if net reserves flip positive in 2026 and reforms hold, sovereign spreads could compress another 300–400bp; conversely, EU export weakness may be over-penalized if tariffs are renegotiated post–USMCA review (July 2026). Watch for unintended winner: Asian contract manufacturers and Mexican suppliers could grab market share faster than models assume.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00