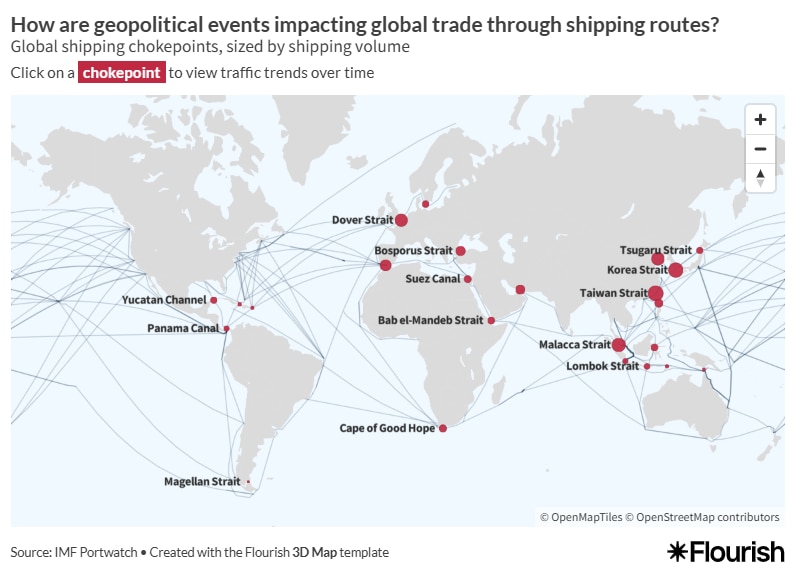

Near-closure of the Strait of Hormuz — which normally handles ~11 million barrels/day of oil and ~140 billion cubic metres of gas — is now disrupting seaborne exports across multiple non-oil commodities. Key impacts include 46% of global urea seaborne trade, ~50% of seaborne sulfur, ~33% of methanol, ~9% of primary aluminium, and ~1/3 of global helium supply, driving tighter availability, upward price pressure, shipping-cost increases and heightened inflationary and food-security risks. The shock threatens inputs for EV batteries and green-hydrogen projects (sulfur, graphite, nickel/cobalt), and is prompting buyers to seek alternative supply routes/regions, increasing near-term market volatility and supply-chain reconfiguration costs.

The most consequential second-order transmission is not an isolated commodity shock but a topology shift in processing-dependent value chains: shortages of refinery by‑products (petcoke, sulfur) and chemical intermediates will compress refiners’ optionality and force downstream processors to re-route feedstock or delay ramp‑ups. That implies a multi‑quarter wedge where battery anode and HPAL nickel projects face input supply friction even if headline metal mines remain operational — expect 2–4 quarters of elevated unit costs for battery cathode/anode integrators and a sustained premium for easily shippable substitutes. Fertilizer tightness will show up with asymmetric timing versus food prices — farmers make application and seed/credit decisions in seasonal windows, so measurable yield impacts and a meaningful grain-price impulse are likelier 6–12 months out, not instant. That timeline creates a predictable calendar trade: buy fertilizer exposure ahead of planting decisions and grain exposure later if fertilizer use data confirms reductions. Logistics shock (longer routes + insurance premia) acts as a regressive tax on low‑margin, bulk‑intensive industries (steel pellets, MEG/polyester, methanol for plastics), compressing processors’ margins while widening owners’ spreads. Shipping and integrated producers with captive freight benefit immediately; standalone processors carrying inventory risk will be pressured on working capital. Catalysts that would reverse these moves are clear: a credible, sustained reduction in regional hostilities (weeks) or rapid insurance-market normalization and alternative routing scale‑up (1–3 months). Conversely, escalation or broader regional closure pushes shortages from quarters to years by shifting long‑run capex decisions and accelerating supply‑side reshoring.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60