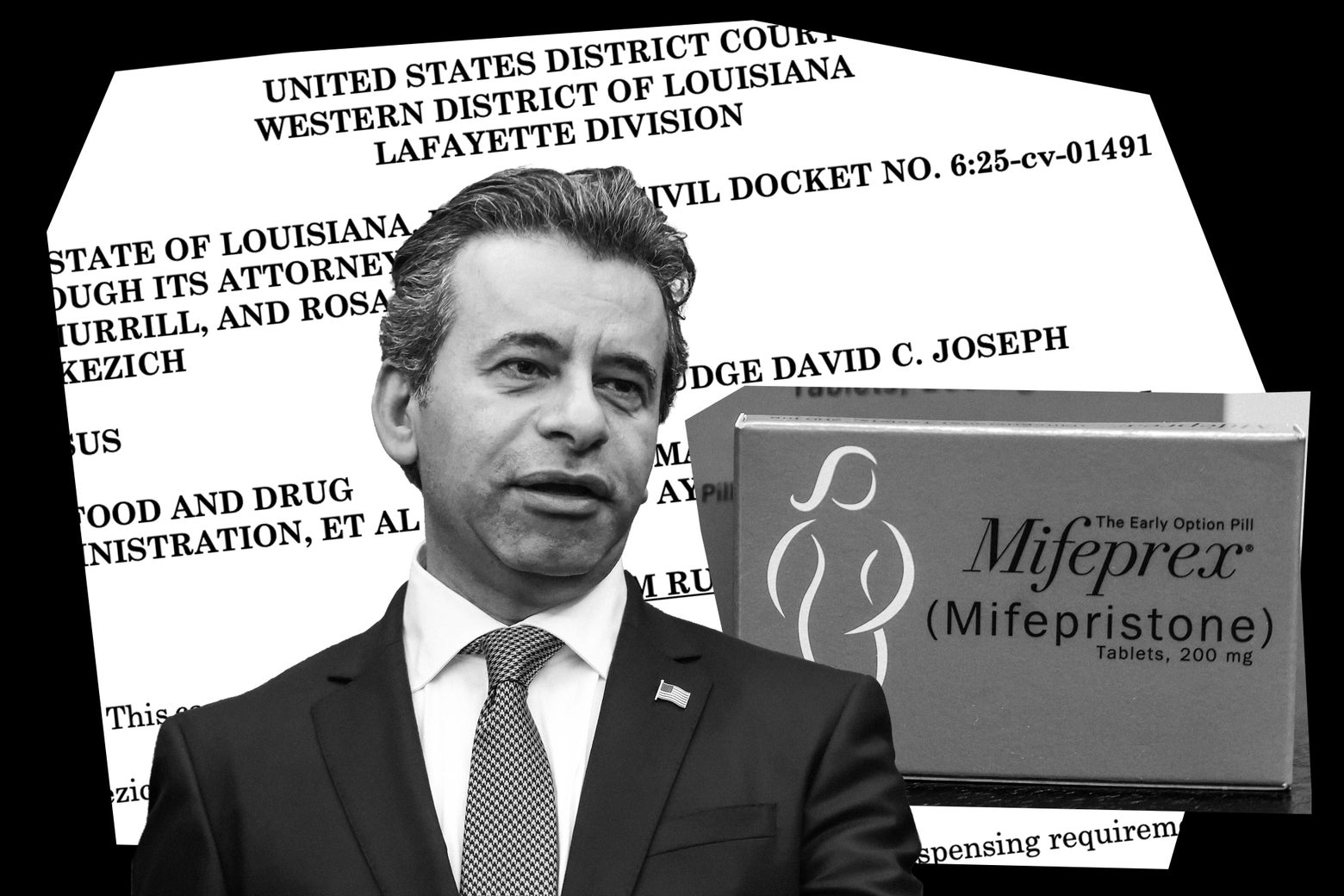

The Supreme Court temporarily stayed the 5th Circuit’s order blocking telehealth access to mifepristone, but the drug remains under active legal and regulatory threat from multiple states and the FDA review process. Louisiana, Texas, Florida, Missouri, Idaho, and Kansas are all challenging mifepristone-related regulation, while anti-abortion groups are pressing for broader restrictions through the courts and the Trump administration. The issue could return to the Supreme Court later this year if the FDA does not reimpose in-person dispensing requirements.

The market read-through is not a direct revenue shock but a regulatory-duration trade: the longer this remains in litigation/agency review, the more optionality shifts toward policy-sensitive healthcare supply chains and away from any pure-play exposed to medication-abortion distribution. The biggest second-order effect is that legal uncertainty raises the cost of capital for telehealth-enabled reproductive health platforms and reinforces a “regulatory overhang” multiple discount across adjacent women’s health names, even if near-term utilization doesn’t change. The deeper risk is timing asymmetry. A court- or FDA-driven restriction would likely be a 3-12 month catalyst, but the market can reprice much faster if the agency signals a reinstatement of in-person dispensing or if the Supreme Court reengages on the shadow docket. The setup is binary: a benign FDA process extends the status quo, while a politicized reversal creates a nationwide precedent that could spill into other drug-class telehealth rules, increasing litigation risk for digital pharmacy and mail-order distribution models. The contrarian angle is that consensus may be underestimating how much this becomes a broader FDA credibility issue rather than a single-product story. If the agency appears to be making a safety decision under political pressure, it weakens the perceived defensibility of other telemedicine-linked prescribing pathways, which could widen risk premia across consumer-facing healthcare tech. Conversely, if the FDA holds firm, the market may quickly price out the headline risk, because the underlying patient demand is politically durable and operationally difficult to suppress. Net: this is less about immediate earnings impact and more about legal optionality, with asymmetric downside for names exposed to telehealth dispensing rules and modest upside for incumbents with diversified in-person care and strong regulatory moats.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35

Ticker Sentiment