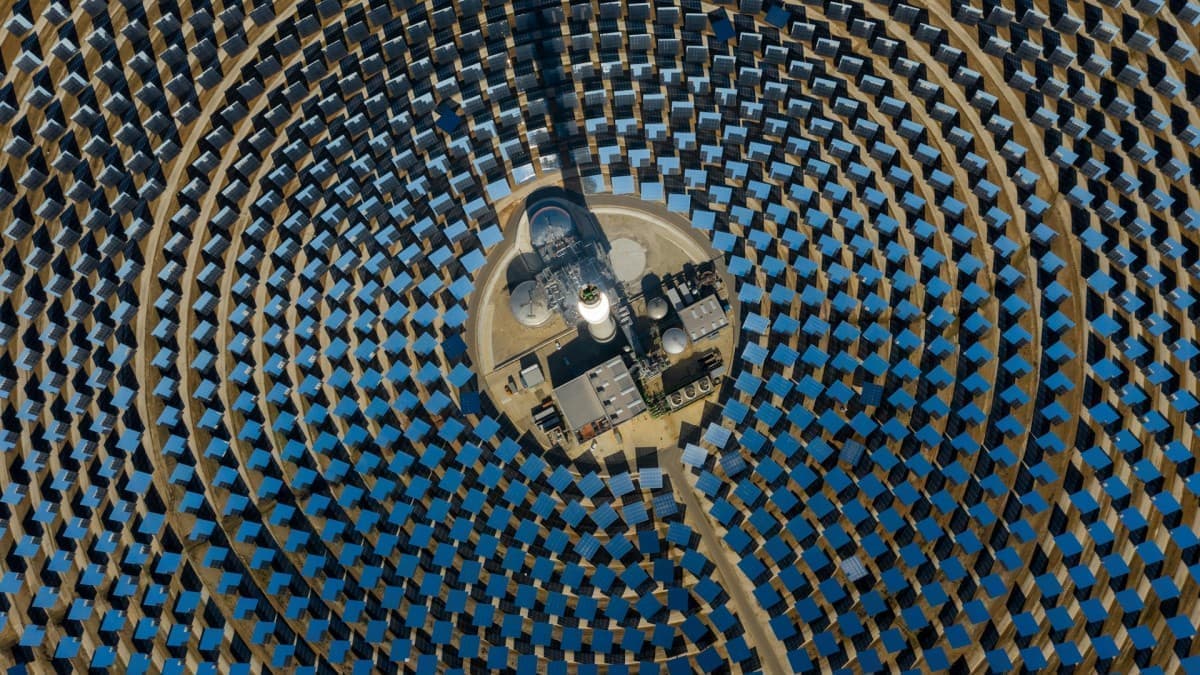

The effective blockage of the Strait of Hormuz — described as the single-largest interruption to global oil trade — highlights vulnerability in oil supply but is not triggering 1970s‑style economic pain due to a more diversified energy mix. Solar capacity has risen from 228 GW (≈1% of global electricity) in 2015 to 2,919 GW (≈9%) in 2025, overtaking nuclear, and could reach ~9,000 GW (>20% of demand) by 2030 in current-growth scenarios. China produces >80% of solar panels, and 63% of emerging markets in Africa, Asia and Latin America now source more power from solar than the United States, underscoring renewables' growing role in energy security and reducing the market impact of geopolitical oil shocks.

The strategic reaction to energy insecurity is shifting capital away from fungible hydrocarbon supply chains toward localized generation and storage — this is not just an electricity mix story but a balance-sheet one: distributed solar converts volatile import-exposure into predictable, financeable asset streams for local lenders and project developers. Expect a multi-year reallocation of project finance (banks, development finance institutions, and green funds) into small-to-medium distributed systems in EMs; that flow will compress short-term merchant power volatility but create a new class of credit risk tied to equipment lifecycles and local regulatory regimes. China’s production dominance creates a concentrated geopolitical choke point: a targeted export restriction or tariff could lift module/polysilicon prices within weeks and force a 12–36 month industrial response (re-shoring, alternate chemistries). That dynamic favors technologies and suppliers with low polysilicon dependence (thin-film, vertically integrated inverters+storage) and accelerates CapEx for downstream balance-of-system players who can vertically integrate supply security. Second-order winners will therefore be inverter and BESS OEMs, regional EPCs with balance-sheet finance capabilities, and commodity suppliers for storage and electrification (copper, lithium, silver). Key risk paths that could reverse the structural view: a prolonged plateau in battery cost declines, accelerated trade barriers that slow deployment economics, or permitting/gridside bottlenecks in major EMs that turn rapid adoption into multi-year backlog. Monitor policy moves (tariffs, domestic content rules) and polysilicon shipment notices as high-probability short-term catalysts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.40

Ticker Sentiment