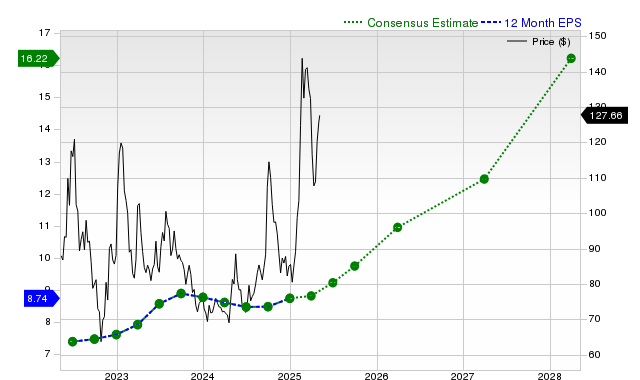

Alibaba (BABA) shares have surged +46.8% over the past month, significantly outperforming the S&P 500, despite mixed analyst sentiment. Current quarter and fiscal year EPS estimates show substantial negative revisions and year-over-year declines, with the current quarter estimate down -52.1% and revised -38.1% in 30 days. However, next fiscal year EPS is projected to rebound +39%, while revenue growth is modest in the near term but accelerates to +11% for the next fiscal year, leading Zacks to rate BABA a 'Hold' (Rank #3) with a 'C' valuation score, suggesting it may perform in line with the broader market.

Alibaba's stock has experienced a significant rally, returning +46.8% over the past month, starkly contrasting with troubling near-term fundamental indicators. Consensus earnings estimates for the current quarter project a severe -52.1% year-over-year decline to $1.03 per share, with analysts having revised this forecast down by -38.1% in the last 30 days. This negative trend extends to the full current fiscal year, where EPS is expected to fall -14.3%. Revenue growth is also sluggish, forecasted at only +1.1% for the current quarter. However, the market appears to be pricing in a sharp recovery, as next fiscal year's consensus EPS estimate indicates a +39% rebound, and revenue growth is projected to accelerate to +11%. This forward-looking optimism is tempered by the company's recent history of missing EPS estimates, doing so in three of the last four quarters, and a neutral Zacks Rank #3 (Hold), which suggests the stock may perform in line with the broader market. Furthermore, a Zacks Value Score of 'C' indicates that its valuation is currently at par with its peers, offering no distinct valuation advantage despite the recent price surge.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment