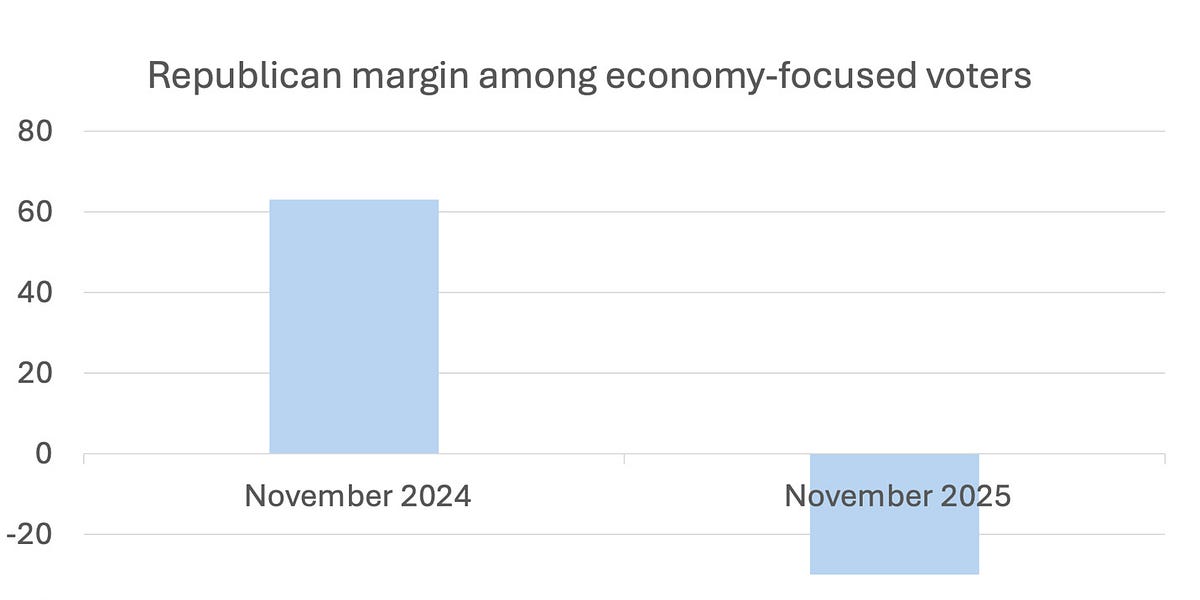

U.S. macro indicators look solid by historical standards — October 2024 unemployment was 4.1% and inflation 2.6%, while by September 2025 unemployment rose to 4.4% and inflation to 3% — yet consumer sentiment has turned sharply negative, now below readings seen after the 2008 crisis and even 1980. Paul Krugman frames this disconnect as a “vibecession,” noting voters blamed incumbents for perceived economic malaise (a 60-point preference for Trump among voters citing the economy in 2024, and a 30-point tilt to Democrats in recent gubernatorial races), and explores multiple explanations including media, partisanship and price-level concerns. For investors, the piece highlights persistent political and sentiment risk despite decent macro fundamentals, implying elevated policy and political uncertainty that could widen risk premia even absent a clear macro collapse.

Market structure will bifurcate: defensive staples (KO, PG), healthcare (JNJ, UNH) and regulated utilities (NEE) gain pricing power as discretionary demand softens and retailers with low-price positioning (WMT, COST) take share from premium discretionary names (AMZN, NKE). Sentiment-driven downdrafts will widen equity risk premia episodically, lifting option-implied vols and flattening liquidity in small/mid caps; commodities tied to cyclical demand (copper, crude) face downward pressure while gold/real assets should act as insurance. Key risks: a contested political outcome or sharp CPI surprise (>+0.5% month) are low‑probability, high‑impact events that would force large policy shifts and spike real rates and credit spreads (IG +100bps, HY +250bps scenarios). Near-term (days/weeks) expect headline-driven vol spikes around polls/CPI; medium-term (3–9 months) earnings misses in consumer cyclicals; long-term (12–24 months) regulatory/tax shifts that re-rate profit margins in tech and finance. Trade implications: favor short-dated volatility and credit protection while rotating into low-beta, cash-generative names; implement relative-value shorts in discretionary vs staples and use options to cap cost of insurance. Monitor two quantitative triggers to act: 1) University of Michigan sentiment <70 for two consecutive months; 2) 10-year Treasury yield move >50bps in 7 days, both signal increased hedging intensity. Contrarian angles: consensus underweights the probability that fundamentals (employment, corporate profits) stay intact — a 10–20% tactical buy-on-weakness in cyclicals (XLY, XLI) is warranted if sentiment mean-reverts by +10 points over 60 days or CPI rolls back below 2.5%, creating asymmetric upside versus crowded defensive positioning.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25