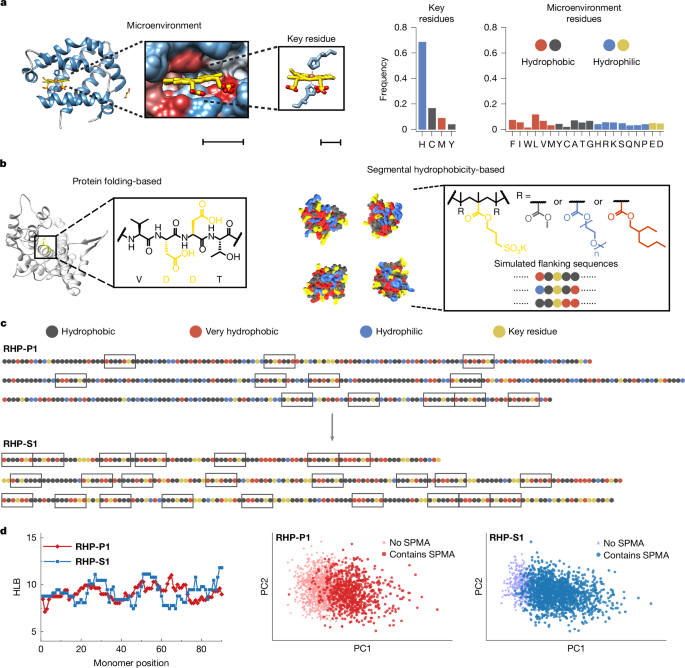

Researchers report in Nature the design of random heteropolymers (RHPs) that mimic enzyme active sites by statistically programming sidechain projections guided by analysis of ~1,300 metalloproteins. The RHPs catalyze reactions including oxidation and stereoselective cyclization of citronellal, operate under non-biological conditions, are compatible with scalable processing and show an expanded substrate scope that includes persistent environmental antibiotics such as tetracycline; the team has filed a PCT patent application on the technology. Commercialization potential exists for catalysis and environmental remediation applications, but no revenue, commercialization timeline, or market-ready product details are provided.

Market structure: Winners will be specialty-chemicals and polymer manufacturers that can supply methacrylate/OEGMA-type monomers and scale RHP production (incremental revenue potential +$200–$600M industry-wide over 3 years if adoption reaches niche industrial catalysts), plus lab-services/vendors (TMO, DHR) and environmental/waste-management firms that win remediation contracts. Losers: pure-play biological enzyme providers and small enzyme-focused biotechs may lose share in non-biological process niches; traditional precious-metal homogeneous catalyst demand could soften. Cross-asset: expect modest upward pressure on methacrylate and specialty monomer prices (5–15% over 6–18 months), small widening of high-yield spreads for early-stage enzyme startups funding scale-up, and limited FX flow to monomer exporters (Asia) as volumes ramp. Risk assessment: Key tail risks include IP/defensive-litigation (PCT patent may provoke blocking suits), scaling failure (30–40% probability RHPs underperform at scale), and regulatory/ESG backlash if RHPs persist in environment (could trigger restrictions within 24–36 months). Immediate market impact is negligible (days); expect pilot commercial deals and volatility in supplier names in 3–12 months; broad industrial adoption likely 18–48 months. Hidden dependencies: availability of specific monomers, contract-manufacturing capacity, and cofactor/heme supply chains; DOD funding materially accelerates deployment in defense/cleanup use cases. Trade implications: Direct plays: establish 2–3% long positions in large specialty-chemicals with catalyst/polymer exposure (e.g., ALB, DOW) and 1–2% long in lab-supplies (TMO) to capture consumables/service upsides over 12–36 months. Pair: long ALB (2%) / short HUN (1%) to express premium for specialty catalysts vs commodity chemicals. Options: buy 9–15 month LEAPS calls on TMO or ALB (25–35% OTM) sized to 1% portfolio risk to capture upside on licensing/M&A. Rotate into Materials/Industrials and away from small-cap enzyme biotech names (reduce by ~50% over 1–3 months). Contrarian angles: Consensus will overestimate speed of displacement — historical parallels (MOFs, artificial enzymes) show 3–7 year commercialization ramps; buyers who price immediate disruption are likely wrong. Conversely, the market may underprice defense and environmental-service demand; a single DOD or municipal contract (>$50–100M) would re-rate suppliers quickly. Watch for ESG/regulatory shock: evidence of persistence or bioaccumulation could flip winners to losers and trigger >20% drawdowns in exposed chemical names. M&A risk: well-capitalized chemical firms could acquire RHP IP for <$500M–$1B, so event-driven upside exists.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment