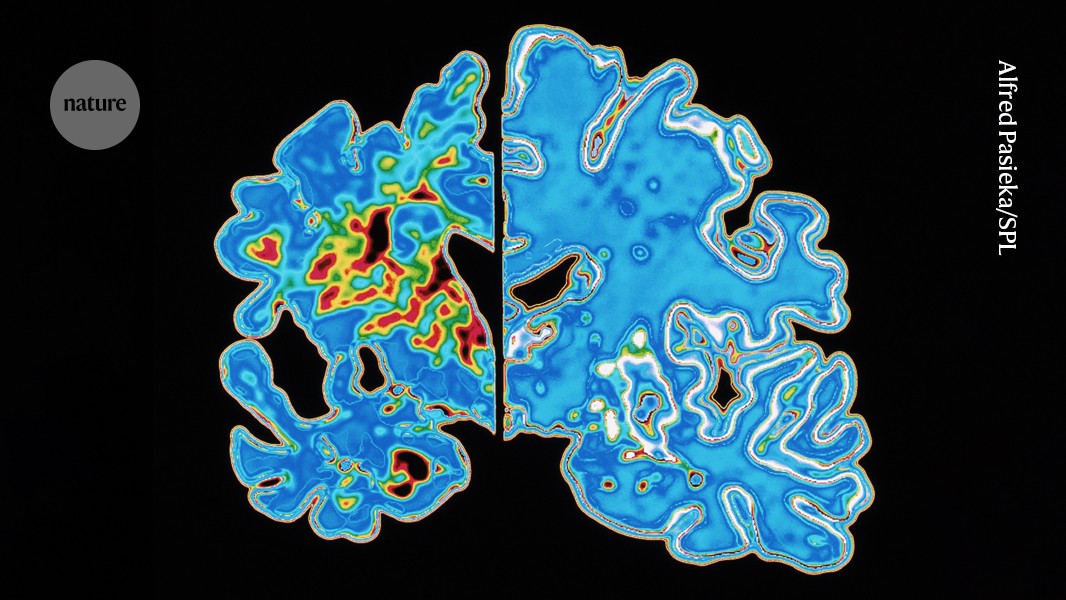

A study published 19 February in Nature Medicine describes a blood-based test that detects an abnormal form of tau protein that accumulates in the brain long before Alzheimer’s symptoms, potentially enabling earlier intervention and a biomarker to streamline clinical trials. The test could lower reliance on costly brain-imaging methods, but validation in larger studies is required and experts currently advise cognitively unimpaired individuals against using consumer in‑home tests.

Market structure: Validated, cheap blood-based tau assays are potential winners — diagnostics labs (Quest DGX, LabCorp LH) and assay specialists (Quanterix QTRX) gain pricing power and volume; Alzheimer’s drug developers (Eli Lilly LLY, Biogen BIIB/Eisai) benefit from cheaper trial enrichment and faster enrollment. PET-imaging vendors and capital-equipment providers (Siemens Healthineers SHL, GE GE) are potential losers if PET volumes decline; I model a plausible 10–30% PET revenue reduction for pure-play imaging over 1–3 years if adoption accelerates. Risk assessment: Key tail risks are regulatory/payer rejection (FDA/FDA-advisory negative guidance or CMS denial of reimbursement), high false-positive rates leading to litigation, or larger validation studies (N>1,000) failing to replicate results. Immediate impact (days–weeks) is limited to volatility in small-cap diagnostics; short-term (3–12 months) hinges on follow-up studies and partnerships; long-term (1–3 years) determines structural substitution of PET by blood tests. Hidden dependencies include lab certification bottlenecks and payer coverage thresholds (price-per-test) that will cap near-term upside. Trade implications: Tactical bias to long pure-play assay developers and large-cap pharmas with Alzheimer’s programs, short selective imaging exposure. Use size control: small initial equity stakes (1–2% portfolio) and option structures to time catalysts (validation study releases, FDA/CMS guidance within 6–12 months). Pair trades (long QTRX or DGX, short SHL/GE) and LEAP call buys are preferred to outright large-cap buys until N>1,000 replication or CMS coverage confirmed. Contrarian view: Market consensus may underestimate payer lag — adoption likely stepwise not immediate, creating a 6–18 month window to buy into validated names before peak euphoria. Historical parallel: liquid biopsy adoption took 2–4 years from proof to routine clinical use; expect similar cadence. Unintended outcomes include overdiagnosis driving regulatory backlash or faster drug demand that re-rates pharma but increases litigation risk for consumer-test vendors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.15