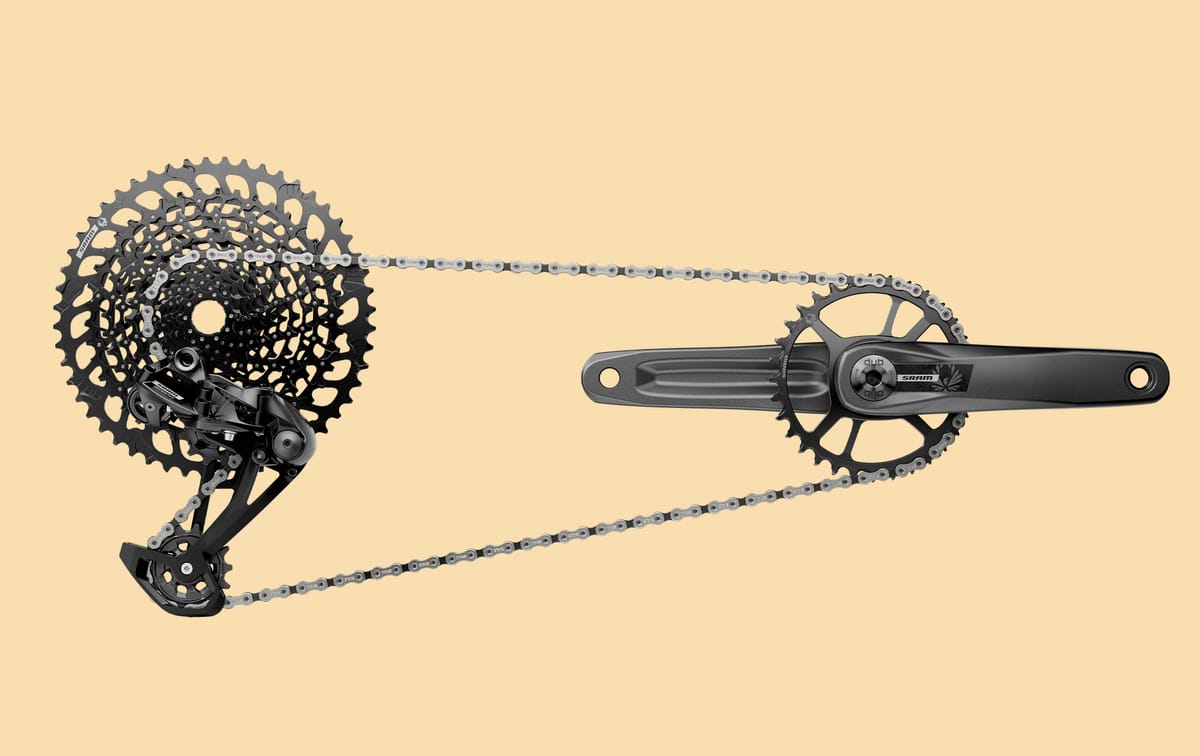

SRAM is streamlining its Eagle mountain bike drivetrain lineup, replacing SX, NX, GX, X01, and XX1 mechanical/AXS with three simplified S-Series tiers: S100, S200, and S500. The new range emphasizes lower SKU counts, backward compatibility, and feature upgrades such as the UDH Half Mount, lighter shifter action, and broader crank-length options. The change is operationally positive but likely limited in near-term market impact.

This is less a product refresh than a channel-clearing event: SRAM is rationalizing a long tail of low-velocity SKUs into a narrower architecture that should improve OEM forecasting, reduce obsolescence, and raise gross margin on the same installed base. The key second-order effect is that it keeps legacy Eagle relevant longer rather than forcing a clean Transmission migration, which protects aftermarket demand and slows frame-level replacement cycles. For NX specifically, the read-through is mildly negative: the value tier becomes a more aggressively managed component business, so unit growth can be preserved while mix and pricing power are capped. The biggest beneficiary is likely not SRAM alone but the bike OEMs and distributors sitting on inventory risk. Fewer variants mean lower working capital and less dead stock, which can stabilize orders after the post-pandemic destock cycle; that matters over the next 1-2 quarters more than the product specs themselves. Competitively, Shimano and smaller drivetrain suppliers face a sharper value-segment fight because SRAM is signaling it will defend entry mechanical share without carrying the same SKU burden that historically weighed on service levels. The contrarian view is that this is incrementally bullish for the category’s profitability but not necessarily for near-term revenue. Simplification usually shows up first as better sell-through, not explosive sell-in, and any OEM re-spec cycle will take 6-12 months to flow through bike builds. If the market is expecting a share grab, the risk is that the launch mostly preserves installed base and improves margin mix rather than accelerating top-line growth. Catalyst-wise, watch channel inventory commentary and OE build schedules into the next two quarters; those will determine whether this becomes a margin story or just a housekeeping event. The main tail risk is that an overly compressed lineup alienates upgrade-oriented riders and specialty retailers, which could cede premium enthusiast mindshare to Shimano or transmission-based alternatives. But if OEM adoption of the simplified tiers is broad, this should modestly improve earnings quality through lower SKU complexity and stronger replacement-part monetization.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15

Ticker Sentiment