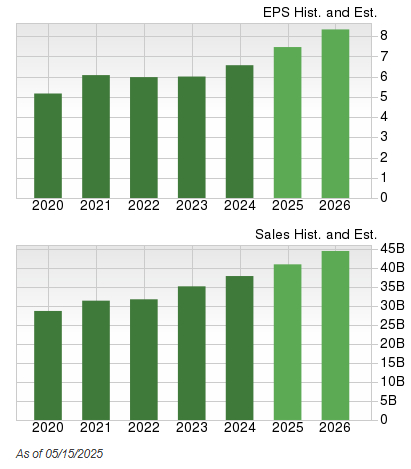

Philip Morris International (PM) is expanding beyond traditional cigarettes, driven by the success of its Zyn oral nicotine pouch, which has captured approximately three-quarters of the tobacco pouch market. PM's EPS has grown consistently, with the last three quarters showing increases of +14%, +14%, and +13% year-over-year, and the company has beaten Zacks Consensus Analyst Estimates in 19 of the past 20 quarters, suggesting continued double-digit EPS growth into 2026.

Philip Morris International (PM) is strategically evolving its business by significantly expanding its smoke-free product segment, with its Zyn oral nicotine pouch brand emerging as a key growth catalyst. This initiative directly addresses shifting consumer preferences towards perceived healthier alternatives to traditional cigarettes. Zyn has achieved substantial market dominance, capturing approximately three-quarters of the tobacco pouch market, and its shipment volumes have more than quintupled over the past five years, propelled by social media trends and its positioning as a less harmful nicotine delivery system. This success in the smoke-free category supports PM's robust financial performance, characterized by consistent year-over-year EPS growth, reported at +14%, +14%, and +13% in the last three respective quarters. Furthermore, Philip Morris has a strong history of exceeding Zacks Consensus Analyst Estimates, achieving this in nineteen of the past twenty quarters. The company's stock demonstrates low volatility, indicated by a beta of 0.14, and has reportedly outperformed over 95% of S&P 500 stocks. With consensus forecasts pointing towards double-digit EPS growth continuing into 2026, bolstered by low operational costs and a healthy cash position, Philip Morris's financial outlook appears favorable.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment