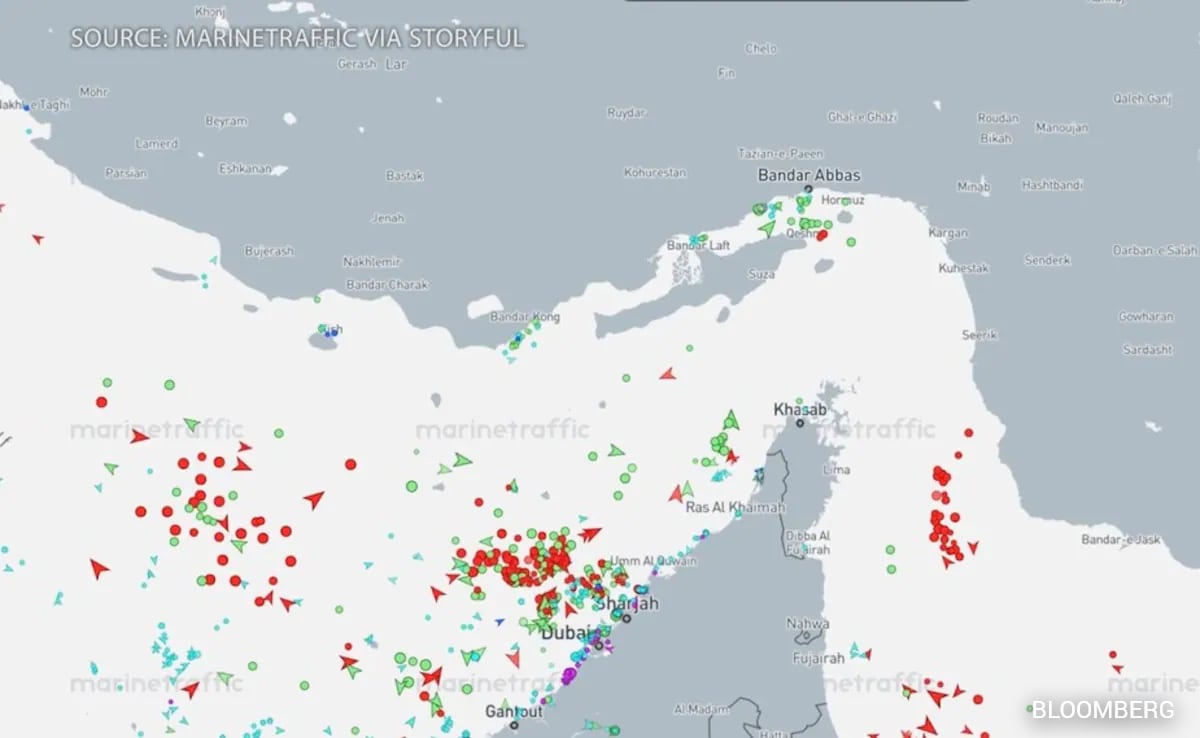

Traffic through the Strait of Hormuz plunged to ~6 vessels/day in March versus ~135/day normal as Iran asserts control, introduces a toll and bans US/Israeli transit. Brent is up close to +60% this month; Iran exported ~1.8m b/d (~+8% vs 2025) even as Iraq exports fell >80% and Saudi volumes are >25% below last year, forcing reroutes through the Gulf of Oman/Red Sea. War-risk insurance premiums have spiked (Persian Gulf ~1.5% of vessel value; Strait up to ~10%), buyers and insurers are seeking waivers and alternative routes, and the disruption represents a persistent, market-wide energy supply shock.

Control of a key chokepoint is creating a durable segmentation of seaborne crude into at least two markets — barrels that can clear Western-insured, public trading channels and barrels that must move via opaque, state-linked corridors. Expect regional pricing differentials to widen and become more volatile: our working assumption is a 20–40% increase in short-term dispersion between Gulf-origin and alternative-route delivered prices over the next 3 months, driven by insurance frictions, longer voyages and counterparty risk premia. The logistics response will be structural, not transitory. Reroutes add voyage miles and idle-time; we model a 5–10% effective reduction in available voyage-equivalent tanker capacity for Persian-Gulf-origin flows over the next 1–4 months, which in turn can push charter rates materially higher and reprice the marginal cost of delivered crude by a few dollars per barrel once insurance and diversion are included. Key catalysts that would reverse the dislocation are concentrated and binary: a coordinated underwriting/backstop from Western reinsurers or a credible, multinational convoy solution could collapse the risk premia in 4–8 weeks, while formal recognition or legal settlements restoring unencumbered transit would take 6–18 months. Tail risks include escalation that expands theatre geography (which would entrench segmentation and force longer-term rerouting) or a rapid normalization through diplomacy that tightens the sell-off window for risk assets. From a macro/credit angle, the shock accelerates revenue reallocation to buyers and shipping counterparties willing to accept higher compliance risk; this increases political leverage for non-Western buyers and makes Gulf fiscal buffers more sensitive to pipeline- and storage-linked bottlenecks. Monitor shipping utilization metrics, tanker TC indices and reinsurance bulletin language as high-frequency signals — changes there will lead price discovery in both energy and insurance markets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75