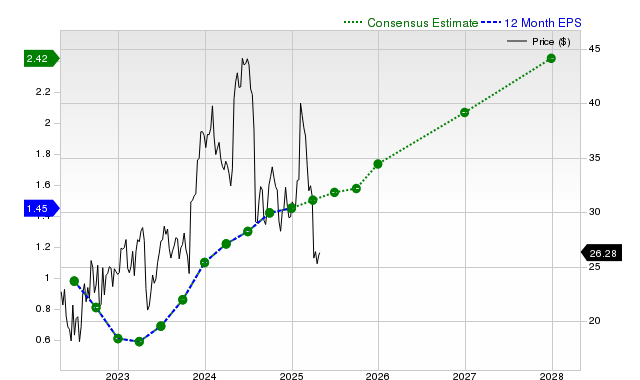

Pinterest (PINS) has recently outperformed the S&P 500, gaining 13.5% over the past month, driven by projected mid-teens percentage revenue growth for the current and next fiscal years. However, despite strong year-over-year earnings growth forecasts, the Zacks Consensus Estimate for current quarter EPS saw a notable 20% negative revision in the last 30 days. The stock holds a Zacks Rank #3 (Hold), suggesting an in-line market performance expectation, and its valuation is assessed as trading at a premium relative to its peers.

Pinterest (PINS) has demonstrated significant recent stock price momentum, delivering a 13.5% return over the past month that outpaces both the S&P 500 composite and its Internet - Software industry peers. This performance is supported by expectations for robust top-line growth, with consensus sales estimates pointing to approximately 14% year-over-year increases for the current quarter, current fiscal year, and next fiscal year. While the company has consistently surpassed revenue estimates over the last four quarters, its earnings profile presents a more complex outlook. A significant negative revision has occurred for the current quarter's earnings, with the consensus EPS estimate falling by 20% in the last 30 days, following an 8% EPS miss in the last reported quarter. This contrasts with a projected 42.6% EPS growth for the full fiscal year. The combination of these conflicting signals contributes to a neutral Zacks Rank #3 (Hold), and a 'D' grade on valuation suggests the stock is currently trading at a premium to its peers, indicating that much of its growth prospect may already be priced in.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment