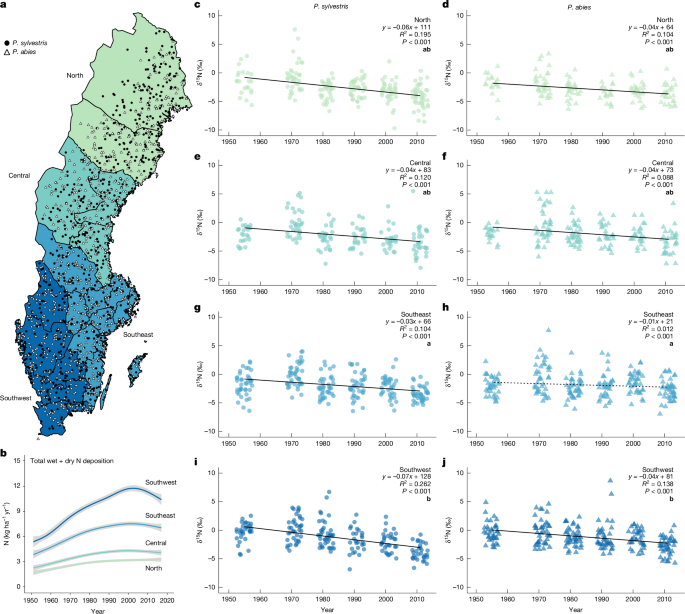

A pan-Sweden analysis of 1,609 archived tree cores (1951–2017 growth increments) shows widespread declines in wood δ15N (≈ −0.01‰ to −0.07‰ yr−1), including in low-deposition northern forests, indicating reduced nitrogen availability. Linear mixed-effects models identify rising atmospheric CO2 as the dominant predictor (P. sylvestris −0.04 ± 0.005‰ δ15N per ppm CO2; P. abies −0.028 ± 0.005‰ ppm−1) with a partial R2m ≈ 0.176 versus ≤0.005 for N-deposition metrics, implying CO2-driven oligotrophication may constrain boreal forest carbon sinks and affect forecasts for carbon sequestration, forestry yields and related carbon-market valuations.

Market structure: Rising-CO2-driven oligotrophication shifts relative winners toward fertilizer producers (NTR, CF) and specialty soil/microbiome biotech (small caps) as commercial forestry may respond with targeted N amendments; winners also include carbon-credit platforms/ETFs (KRBN) as verified sinks face downward revision and credit scarcity. Losers are unmanaged boreal timber producers and some pulp/paper producers whose long-run yield projections and carbon revenue may be marked down, creating upward pressure on lumber/pulp spot prices but downward revisions to sustainable-yield-based valuations. Risk assessment: Tail risks include regulatory bans on large-scale fertilization (environmental/acidification concerns), rapid re-pricing of forest carbon offsets if sink estimates are revised, and compound disturbances (pests/drought) that amplify supply shocks; probability low-medium but impact high (10–30% cashflow swings). Timeline: near-term (0–3 months) low market impact; short-term (3–18 months) repricing via earnings guidance and policy debate; long-term (2–10 years) structural shift in land carbon accounting and commodity supply-demand. Trade implications: Tactical opportunities—buy fertilizer exposure (NTR, CF) and carbon-credit ETFs (KRBN); consider call spreads (12–18 month) on NTR/CF to cap premium. Pair trade: long CF (2–3% portfolio) vs short Weyerhaeuser (WY) (1–2%) to capture fertilizer tailwind vs timber-growth risk. Use puts on timber REITs (WY) as downside insurance if EU LULUCF or corporate guidance revisions occur within 6–12 months. Contrarian angles: Consensus underestimates price support from constrained timber supply—timberland land values may hold or rise even as biological growth slows, so outright shorting broad timberland without catalyst risk is dangerous. Historical parallel: mid-20th-century fertilizer tech reversed nutrient limits—watch for rapid adoption of soil amendments/mycorrhizal biotech that could blunt the thesis and cap fertilizer upside within 3–5 years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25