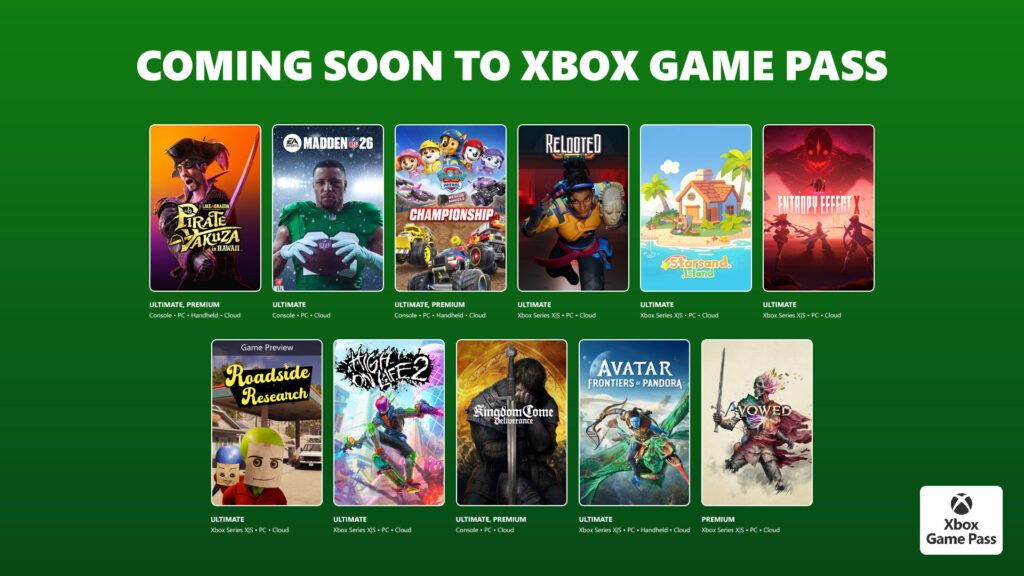

Microsoft announced a slate of games arriving on Xbox Game Pass in the first half of February 2026, including Avowed (Game Pass Premium), Like a Dragon: Pirate Yakuza in Hawaii, High on Life 2, Kingdom Come: Deliverance and several other titles across Ultimate, Premium and PC tiers with specific mid-February release dates. The additions—together with only one departure (Madden NFL 24 on Feb. 15)—enhance Game Pass content breadth and could modestly support subscriber engagement and retention for Microsoft’s gaming division, though the update is unlikely to materially move financials or markets.

Market structure: Microsoft (MSFT) is the clear direct beneficiary — incremental Game Pass content, especially high-profile RPGs (Avowed, Kingdom Come, Like a Dragon), improves subscriber value and retention, which should translate into modest ARPU upside: +1–3% over 3–6 months if churn falls by 25–75 bps. Traditional boxed-game retailers (GameStop GME) and single-purchase revenue models face further secular pressure as live-subscription monetization substitutes for full-price buys; expect declining physical sales share by ~5–10% annually in core markets. Risk assessment: Tail risks include antitrust scrutiny over platform/content bundling and rising third‑party licensing costs (a 20–40% increase in content payouts could compress Xbox margins materially). Near term (days–weeks) stock moves will be sentiment-driven and muted; over quarters (3–12 months) the real test is whether content additions convert to measurable subscriber growth and margin retention; watch next 90-day subscription metrics and quarterly consent/licensing filings. Trade implications: Favor large‑cap exposure to MSFT via equity or defined‑risk options — target a 2–3% portfolio long in MSFT with 3–6 month time horizon; hedge by reducing exposure to physical retail gaming (GME) by 20–40%. Consider pair trade long MSFT vs short GME or other brick‑and‑mortar retailers to isolate secular streaming/sub model capture; use call spreads to cap cost if implied vol is rich near launches. Contrarian view: Consensus focuses on subscriber upside but underestimates rising content cost and publisher pushback; historically (Netflix 2011–2016) content-driven subscriber growth initially lifts multiples but later compresses margins as licensing escalates. If MSFT cannot limit per-title payouts or convert Game Pass users to higher‑margin services, upside is capped — a breach of +2% sequential ARPU improvement should be required to justify adding more than 3% weight over 6 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment