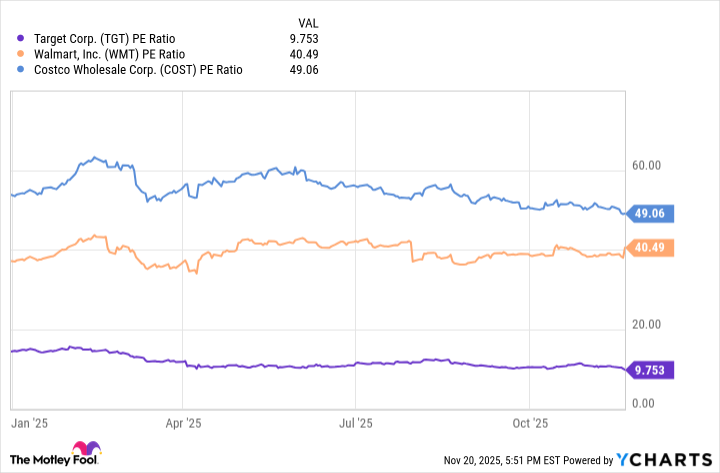

Target reported continued weakness through fiscal 2025 with $74 billion in net sales for the first nine months (ended Nov. 1), down 5% year-over-year, and net earnings just under $2.7 billion, down about 11% YoY; the stock trades at roughly a 10x P/E. Management change (COO Michael Fiddelke named CEO) and customer backlash over political stances have weighed on sentiment, but the company generates roughly $3.4 billion in trailing-12-month free cash flow, pays a $4.48 annual dividend (≈5.4% yield) that cost under $2.1 billion, and operates nearly 2,000 stores—factors the piece highlights as supporting a contrarian investment case.

Market structure: Target’s Q3 weakness (sales -5% YTD, net earnings -11%, FCF ~$3.4bn vs dividend cost ~$2.1bn) disproportionately benefits value-focused chains (WMT, COST) that capture budget-conscious spend; suppliers of private-label and mid-tier apparel face order moderation. Target’s ~2,000 stores preserve distribution scale and localized pricing power, but expected share shift toward Walmart/Costco will compress Target’s margin premium and force higher promotional intensity over the next 2–4 quarters. Risk assessment: Tail risks include a forced dividend cut (low probability but high impact if FCF falls < dividend cost + 20%), activist tax on governance, or a botched CEO transition that triggers inventory/strategy missteps. Immediate horizon (days): elevated IV and event risk around investor commentary; short-term (weeks–months): holiday comps and guidance will be decisive; long-term (4–12+ months): recovery hinges on stabilizing same-store sales and product-mix shift back to higher-margin categories. Trade implications: Tactical exposures should target asymmetric payoffs — small-to-medium long base plus downside protection. Entry triggers: accumulate on price weakness to a level implying yield ≥5% (current ~5.4%) or price <~$70 (set as illustrative buy threshold), use 3–6 month protective puts or sell cash-secured puts 10% OTM to acquire stock; consider long TGT vs short WMT pair for relative rebound play over 6–12 months. Contrarian angles: Market may be over-discounting franchise value and dividend durability — if Target stabilizes comps by mid-2026, upside could be 25–40% as multiple re-rates from P/E ~10 toward peers. Risks to that thesis: dividend maintenance could starve reinvestment, and cultural/brand erosion from recent politics/management changes may create multi-year share loss rather than a quick snapback.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.12

Ticker Sentiment