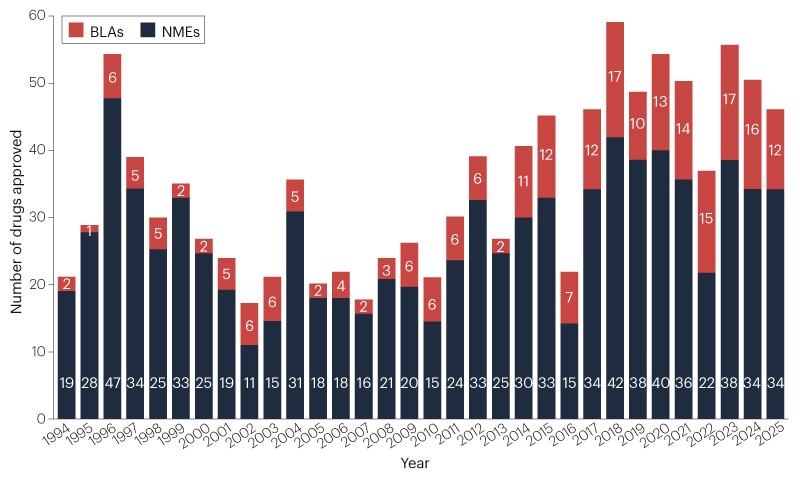

The FDA’s CDER approved 46 new therapeutic agents in 2025 (bringing the 5‑year average to 48 versus a historic 36), with oncology accounting for 16 approvals (35%) and several first‑in‑class and modality breakthroughs (eg, adnectin, PROTACs, novel ADCs). Analysts flag multiple potential blockbusters — notably Merck’s subcutaneous pembrolizumab combination with projected peak incremental sales of $9.3B (pembrolizumab $32B in 2025), Daiichi Sankyo’s datopotamab deruxtecan ($5.4B peak), Insmed’s brensocatib ($6.3B peak) and Vertex’s suzetrigine ($3.7B peak) — while BCG/Evaluate median peak sales for new approvals are ~$600M and mean ~$1.2B. The approvals come amid major FDA upheaval (over 18% CDER/CBER staff turnover in nine months, five CDER directors) and controversial policy shifts (CNPV pilot, moves toward single pivotal trials and reduced animal testing), increasing regulatory uncertainty for investors assessing biotech exposure and product commercialization risk.

Market structure: 2025 approvals concentrate commercial upside in large-cap oncology and platform players (Merck’s Keytruda Qlex — $9.3bn incremental peak cited; pembrolizumab $32bn base) and first-in-class non-oncology winners (INSM brensocatib ~$6.3bn peak). Small developers with single-product franchises or manufacturing-fill finishes (REPL, small gene-therapy names) face increased selection pressure; oral disruptors (Merck oral PCSK9) create asymmetric downside for injectables. Competitive dynamics will shift pricing power to incumbents that bundle delivery advantages (subcutaneous PD1) and to platform owners of validated modalities (ADCs, BTK inhibitors). Risk assessment: regulatory politicization and the CNPV pilot raise tail risk of accelerated approvals followed by safety-driven label changes or market withdrawals — a 10–30% downside scenario for affected small caps within 6–18 months. Operational risks (fill–finish failures, supply chain) are single-point-of-failure events for clinical-stage biotechs; watch third-party CMO exposures and CRL frequency. Key catalysts: FDA decisions listed for H1–2026 (Replimune Apr, Merck PCSK9 filing Apr) and payer coverage determinations in 3–12 months. Trade implications: prioritize large-cap pharma with validated cash flows (MRK, GSK, ABBV, NVS) and selective exposure to INSM; avoid or hedge small-cap biotechs with recent CRLs (REPL) and concentrated manufacturing risk. Use directional options to express convexity — e.g., buy 9–12 month call spreads on MRK and 12–18 month LEAPs on INSM, sell short-dated premium on names with IV>70%. Rotate 20–30% of small-cap biotech weight into vaccines and established immuno-oncology over 1–3 months to lower idiosyncratic risk. Contrarian angles: consensus underestimates the pace at which payer/public pressure will compress prices for convenience-differentiated products (adnectins, subcutaneous mAbs) once oral alternatives arrive — a 30–50% revenue risk over 3–5 years for niche injectables. Conversely, the market may have over-penalized quality mid-caps after CRLs; selective rehabs (if manufacturing remediated) can produce 2x returns within 6–12 months. Historical parallel: 2015–2017 accelerated oncology approvals showed 40–60% retracements on later safety signals — prepare asymmetric hedges.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.06

Ticker Sentiment