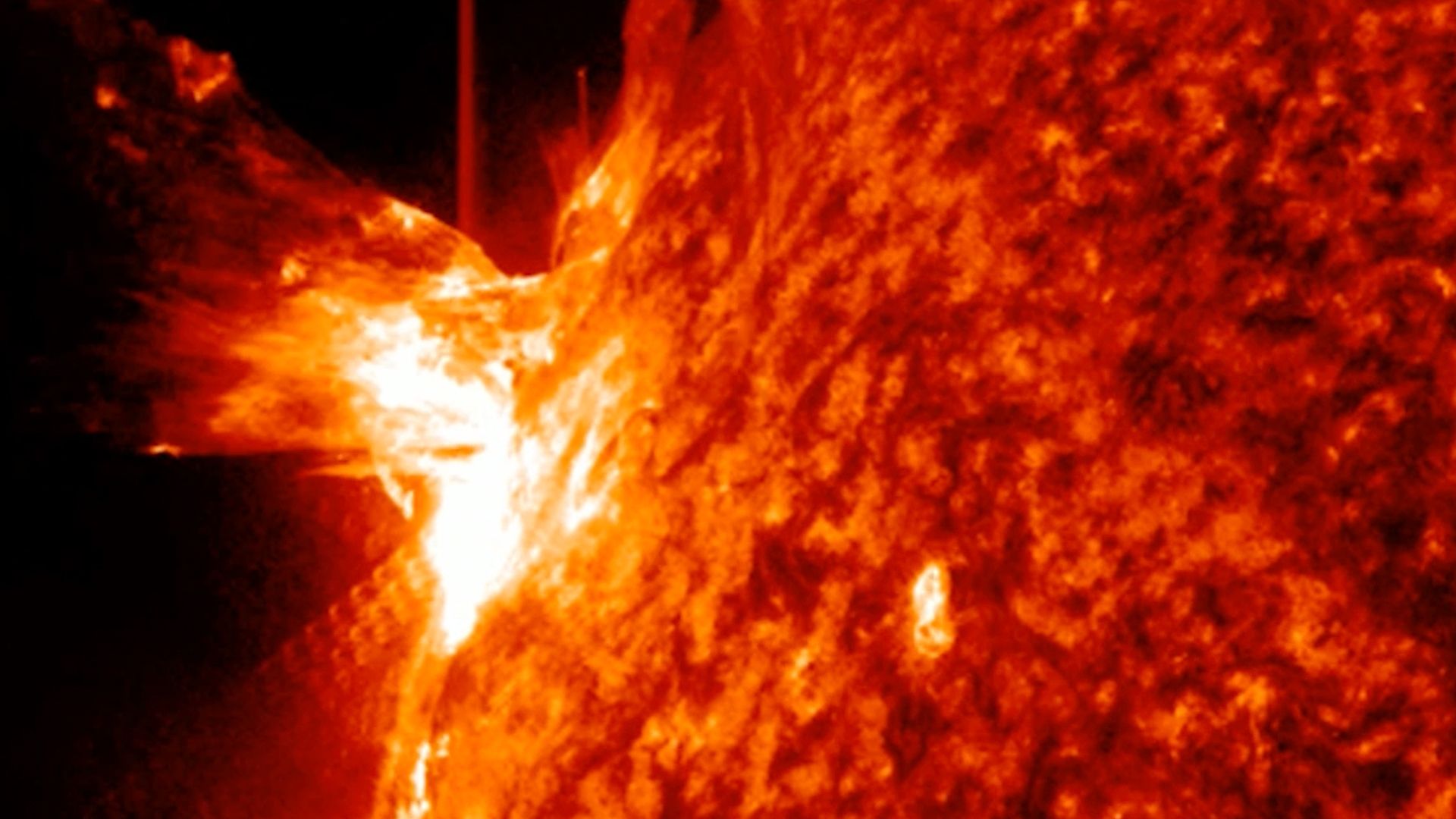

A strong X1.9-class solar flare from emerging sunspot region AR429 caused an R3 radio blackout across Australia and parts of Southeast Asia and produced a rapid partial-halo CME that is not Earth-directed. A much larger, complex sunspot cluster (AR4294) is rotating into view and NOAA forecasters expect continued M‑class activity with a slight chance of additional X‑class flares Dec. 1–3; geomagnetic conditions should remain mostly quiet until a negative-polarity coronal hole stream may drive minor G1 storming around Dec. 3. Investors should note limited near-term market impact but monitor risks to communications, satellite services and dependent infrastructure if AR4294 produces Earth-directed CMEs.

Market structure: Winners are suppliers of hardened communications, satellite operators and defense primes (L3Harris LHX, Raytheon RTX, Iridium IRDM) and grid-infrastructure vendors (ABB ABB, Siemens SIEGY) that can sell retrofits; losers in the near term include polar-route airlines (UAL, AAL) and operators reliant on HF/shortwave comms. Expect a 3–7% reallocation of utility/defense capex toward hardening over 6–18 months, lifting pricing power for specialized components and rare-earth magnets; commodities exposure tilts toward copper/steel and specialty alloys used in transformers and shielding. Risk assessment: Tail risk of a Carrington-class event remains <1%/yr but produces catastrophic multi-week grid/satellite outages; a more realistic near-term tail is a 5–15% chance over the next 7–10 days that AR4294 produces an Earth-directed CME causing regional HF blackouts and localized grid disturbances. Hidden dependencies include single-source transformers with 6–24 month lead times and GPS-dependent logistics; trigger metrics to watch are NOAA Earth-impact probability >30% and Kp index sustained >6. Trade implications: Tactical trades should be bifurcated: short-duration hedges for immediate volatility and strategic longs for expected capex. Near-term: buy 1-month OTM puts on selected airlines to hedge polar reroutes; medium-term: establish 2–3% long positions in RTX/LHX and 1–2% in ABB/NEE for 6–24 months; allocate 1–2% to GLD as a tail hedge and consider 3-month call spreads on IRDM or MAXR to play satellite demand. Contrarian angles: The consensus overstates systemic disruption risk to markets (airline revenue hits likely <5% quarterly) while underpricing multi-year upside for infrastructure vendors where replacement lead times create pricing power. Historical storms (2003–2012) caused brief operational disruption but led to sustained capex cycles; unintended consequence: accelerated government spending could crowd out small suppliers but benefit large integrators—favor scale and service-capable names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.10