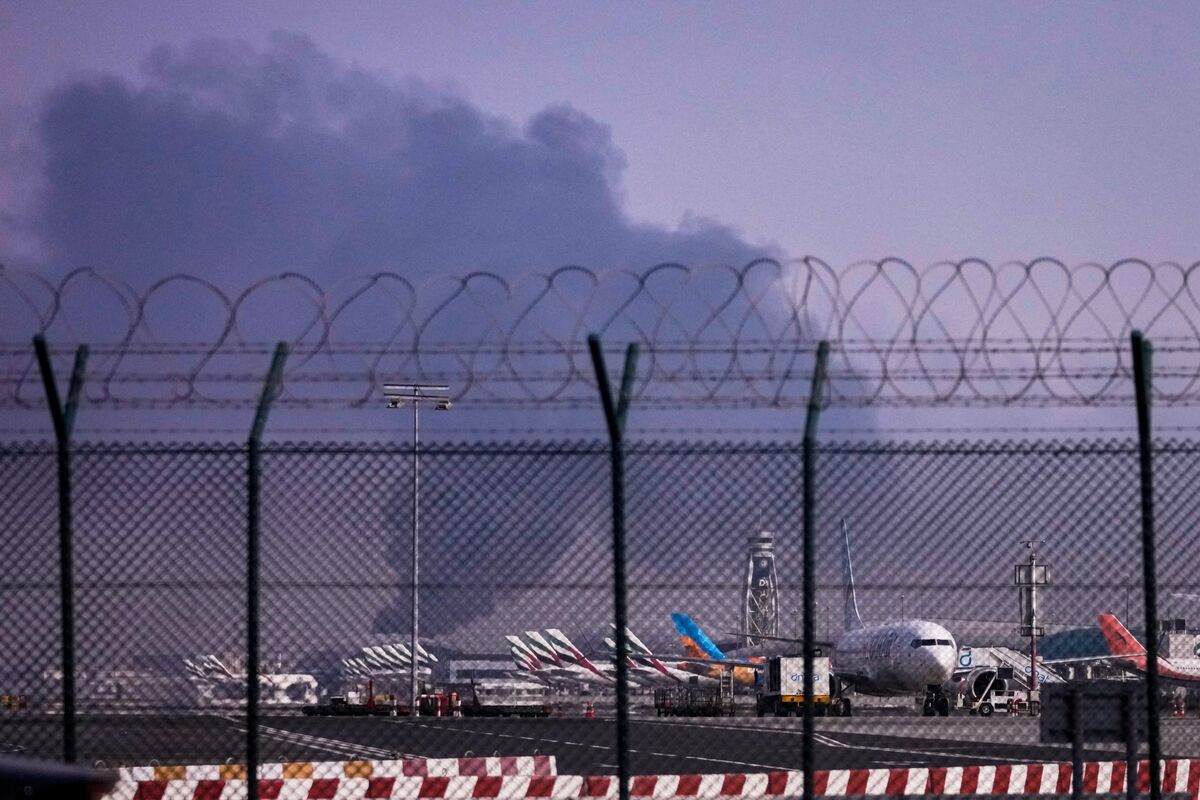

Gulf powers Saudi Arabia and the UAE are weighing military participation alongside the US and Israel if Iran attacks critical Gulf power or water infrastructure. Iranian strikes have already hit ports, energy facilities and airports, raising the risk of broader regional conflict and potential oil supply disruptions. The development increases risk-off dynamics and could materially elevate volatility and risk premia in energy and shipping markets.

The immediate non-linear channel is maritime frictions: elevated war-risk premiums + route diversion materially increases time-on-water and unit shipping costs for crude and refined product flows. Expect spot tanker rates (VLCC/aframax) to rise 20-80% within weeks of any perceived Gulf chokepoint closure; that shock amplifies refinery feedstock mismatches and forces drawdowns of coastal product inventories, not just crude barrels.

A sustained regional security premium in oil is the most direct transmission to markets — a loss of 0.5-1.0 mb/d in effective export capacity historically translates into a $5-15/bbl move in Brent over 1-3 months in a tight market. Political responses (diplomatic de-escalation, coordinated SPR releases, or rapid insurance-market normalization) can unwind >50% of that premium inside 30-90 days, making time-limited hedges optimal versus outright long duration exposure.

Defense and insurance are second-order beneficiaries with asymmetric timing: contractors win multi-year procurement but revenue lags awards by 6-24 months, while insurance/reinsurance repricing happens immediately and can lift underwriting margins in one quarter. Key monitoring triggers that should alter positioning are: measurable disruptions to power/water grids, formal coalition defense commitments, LNG/major-port closures, and a >50% jump in Gulf war-risk insurance premiums — each is a high-probability catalyst to re-rate positions in 2-8 weeks.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65