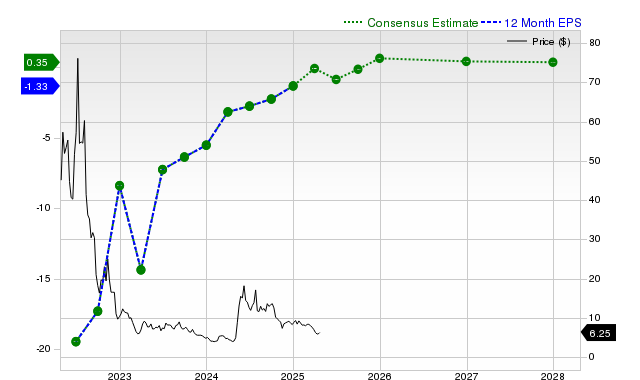

Novavax (NVAX) remains a mixed case for investors: the stock is down 23.8% over the past month while Zacks assigns a Rank #3 (Hold). Zacks' consensus expects a current-quarter loss of $0.58 (‑13.7% y/y) with the 30‑day EPS estimate revision down 16.6%, but the current fiscal year consensus is $2.14 (+274% y/y) and last quarter reported revenue of $70.44M (‑16.6% y/y) and EPS of ‑$0.62, both comfortably beating consensus (revenue surprise +77.9%, EPS surprise +42.6%). Revenue and EPS forecasts show divergence across fiscal years (current year revenue est. $1.06B +54.7%; next year $286.85M ‑72.8%), and valuation receives a C grade, implying the stock may trade in line with peers absent clearer fundamental upside.

Winners will be large-cap, diversified vaccine/pharma names (e.g., PFE, MRNA) and contract manufacturers that can win share as smaller players struggle for procurement dollars; losers are single-product vaccine biotechs and their suppliers as pricing and volumes are negotiable with governments. Competitive dynamics favor firms with integrated commercial channels and multi-year government framework agreements, compressing pricing power for niche entrants and increasing the probability of deal-driven revenue volatility. Immediate tail risks center on headline-driven contract cancellations or safety/regulatory setbacks that can move price sharply in days; medium-term risk is a revenue cliff and dilution over 3–12 months if backlog fails to convert, while long-term outcomes hinge on consolidation or niche commercialization over 12–36 months. Hidden dependencies include reliance on a small number of government buyers, indemnity/advance purchase terms, and third‑party fill/finish capacity that can create asymmetric downside. Tactically, volatility and binary catalysts (earnings, contract awards, FDA meetings) favor defined-risk option structures and small directional allocations: asymmetric payoff hedges outperform naked exposures over 30–90 days. Pair trades substituting large-cap vaccine exposure (long PFE) against idiosyncratic small-cap risk (short NVAX) reduce sector beta while targeting alpha from margin contraction and funding dilution. Consensus may underestimate the speed of government procurement resets and over-penalize upside from a single new contract; conversely, the market can also be pricing in a realistic ‘cliff’ that warrants disciplined downside protection. Historical parallels (post-pandemic vaccine demand shocks) show either rapid re-rating on contract wins or prolonged underperformance until M&A; position sizing should assume binary outcomes and limited liquidity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment