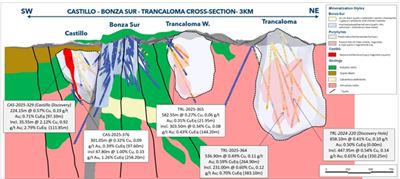

Lundin Gold reported near‑mine porphyry exploration results at its Fruta del Norte concessions in Ecuador, including a new porphyry discovery (Chontas) that extends the Sandia–Trancaloma corridor to at least 10 km. Highlight intercepts include SND‑2025‑383 with 603.25 m at 0.79% CuEq (including 322.30 m at 1.08% CuEq) and TRL‑2025‑340 with 945.05 m at 0.43% CuEq; Castillo returned a higher‑grade semi‑massive sulfide interval of 100.8 m at 0.80% CuEq (including 47.8 m at 1.26% CuEq). Multiple rigs are active and the systems remain open along strike and at depth, indicating meaningful district‑scale exploration upside that could affect Lundin Gold’s resource growth thesis and investor valuation expectations.

Market structure: Lundin Gold (LUG.TO / LUGDF) is the primary beneficiary — discovery expands near‑mine copper optionality and creates a >10 km porphyry corridor that materially increases takeover and re‑rating optionality versus peers. Short‑term winners also include copper explorers and service providers; pure high‑grade gold peers with no copper exposure could relatively underperform. Net impact on global copper supply is negligible near‑term but increases long‑term optional supply optionality, which markets will price only as resources convert to MRE/PEA (12–24 months). Risk assessment: Key tail risks are political/regulatory action in Ecuador (10%+ shock probability over 12 months), metallurgical/recovery setbacks (20–30% chance large zones downgrade after metallurgical test work), and dilution from accelerated drilling/capex. Immediate (days) risk = sentiment chop (±10–25% moves); short term (weeks–months) hinges on follow‑up drills and QA/QC; long term (12–36 months) depends on MRE conversion, PEA and permitting. Hidden dependencies: power/water grid access, metallurgy (Cu/Au recovery split), and community/royalty negotiations. Trade implications: Tactical: establish a 2–3% long position in LUG.TO within 5 trading days, target +25–40% over 6–12 months, trim at +20–30% or on a confirmed MRE miss; place stop at −30% or on a confirmed adverse Ecuador policy. Options: buy Mar‑2027 LEAP calls sized 0.5–1% of portfolio to capture upside with defined risk; consider a 6–9 month call spread if IV spikes. Relative play: pair long LUG.TO vs short GDX (equal notional) to isolate Lundin exploration upside while hedging gold/copper beta. Contrarian angles: Consensus understates dilution and capex risk from district‑scale follow up — a large multi‑rig program can trigger >10% equity raises within 6–12 months, compressing near‑term returns. Conversely, market may underprice takeover risk: a strategic bid from a major copper/gold producer within 12–24 months could add 20–50% takeover premium if MRE shows multi‑100s Mt copper‑gold envelope. Monitor copper <$3.50/lb or Ecuador fiscal proposals as hard stop signals to exit.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.55

Ticker Sentiment