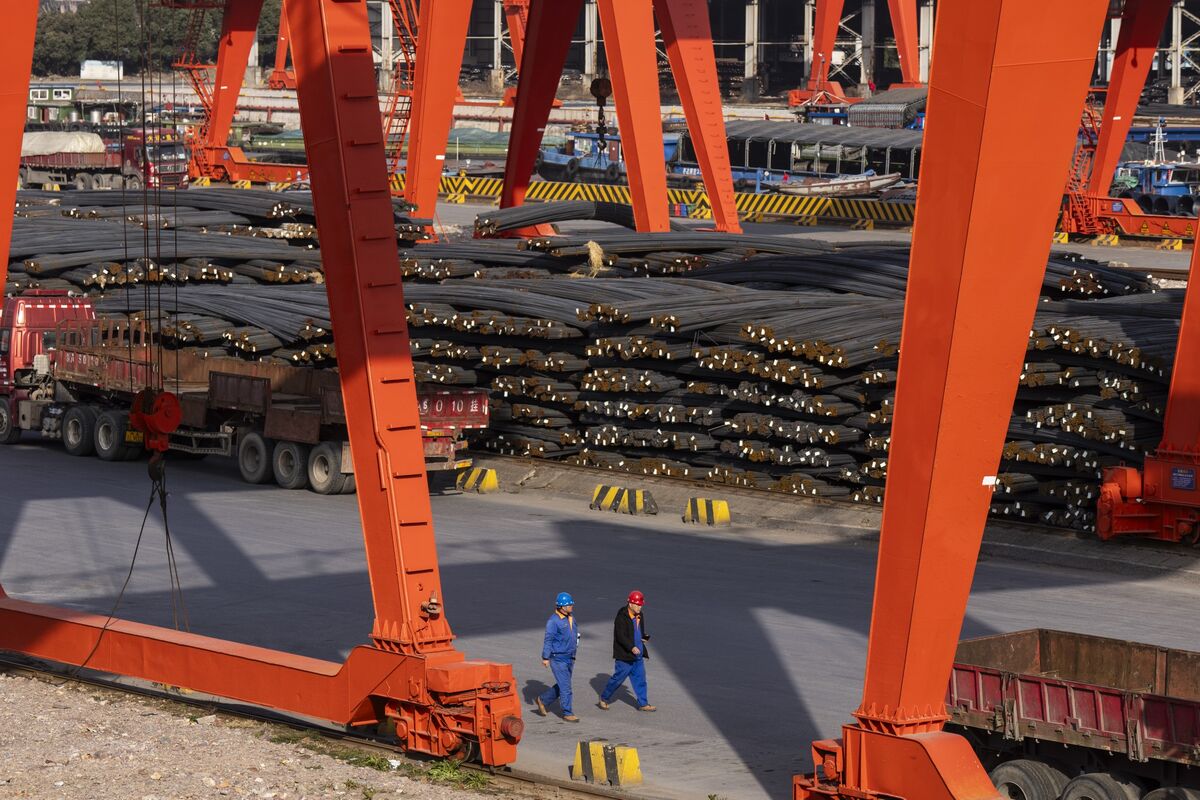

Chinese steelmakers are showing signs of recovery, narrowing losses and improving their outlooks after a challenging period marked by property market weakness. This improvement is driven by government initiatives to address oversupply and resilient export volumes despite global trade curbs, suggesting a potential stabilization in the world's largest steel producing sector.

The Chinese steel sector is exhibiting nascent signs of a cyclical recovery after a period of significant distress. Last year, the industry was characterized by widespread losses, primarily driven by faltering demand from China's ailing property market. The current landscape shows a material improvement, with steel mills reporting narrowing losses and executive sentiment turning less pessimistic. This turnaround is supported by two key factors: proactive government measures aimed at reducing systemic oversupply and the resilience of steel export volumes, which have held up despite an increase in global trade barriers. The combination of state-led industry consolidation and sustained international demand suggests a potential stabilization in fundamentals for the world's largest steel-producing nation, even as domestic real estate headwinds persist.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.50