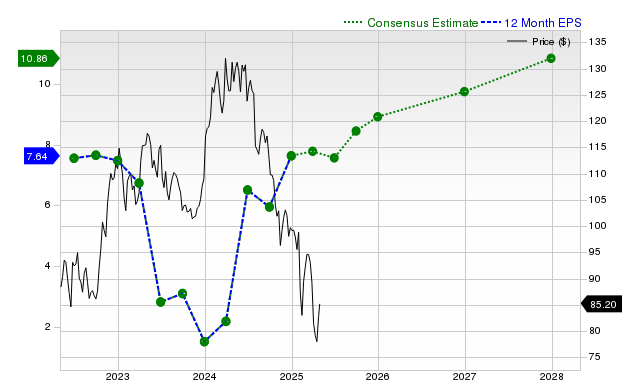

Merck reported last-quarter revenue of $17.28 billion (+3.7% YoY) and EPS of $2.58 (versus $1.57 a year ago), topping consensus revenue by +1.24% and EPS by +9.32%; shares have risen ~20.9% over the past month. Zacks shows mixed analyst estimate revisions — current-quarter EPS expected $2.07 (+20.4% YoY) with the 30‑day consensus down 5%, fiscal-year EPS $8.98 (+17.4%) and next fiscal year $8.81 (−1.8%) — producing a Zacks Rank #3 (Hold) even as Merck earns an A on Zacks' value score. The data suggest solid recent operational performance but tempered near-term estimate revisions, implying measured investor optimism rather than a definitive bullish catalyst.

Market structure: Merck (MRK) benefits directly from resilient large‑cap pharma demand and yield‑seeking flows into defensive healthcare; competitors with weaker pipelines or higher valuations (eg, small‑cap biotech) are relative losers as capital re‑allocates. Pricing power is stable short term because blockbuster franchises (concentrated revenue sources) keep gross margins high, but market share risks from biosimilars or new entrants could materialize over 12–36 months. Cross‑asset: a sustained MRK rally tightens IG credit spreads slightly for large pharmas, reduces equity implied volatility in the sector, and should have minimal FX or commodity impact aside from USD sensitivity on reported revenues abroad. Risk assessment: Tail risks include adverse FDA decisions, major trial failures, or sudden biosimilar litigation losses that could wipe out 15–30% of market cap; political/price‑control reforms pose multi‑year downside. Immediate (days) risk is momentum reversal after a 20% month move; short term (weeks–months) risk centers on quarterly guidance and estimate revisions (-6.6% next‑year EPS change recently); long term (quarters–years) hinges on patent cliffs and pipeline readouts. Hidden dependencies: concentrated product mix, reimbursement dynamics, and FX exposure; key catalysts are upcoming earnings, FDA milestones, and competitor biosimilar launches within 60–180 days. Trade implications: Maintain modest long exposure to MRK as a defensive/value play but size to 1–2% of portfolio and scale into 5–10% pullbacks within 4 weeks; target 12–24 month total return 10–15% and trim at +20% or on guidance deterioration >5%. Implement pair trade: long MRK vs short PFE equal notional (3–6 month horizon) to isolate company‑specific upside, and use 3‑6 month protective puts (3%–5% OTM) if exposure >2% AUM. Use options: buy 6‑9 month call spreads (limit cost) or sell covered calls if long to harvest premium and cap upside. Contrarian angles: Consensus focuses on momentum and recent beats while underweighting next‑year EPS debias (estimates down ~6.6% month) and execution risk from concentrated franchises; the 20% one‑month rally may be overbought relative to fundamentals. Historical parallels: post‑beat rallies in large pharmas often mean‑revert 8–15% within 3 months absent upward guidance revisions. Unintended consequence: crowding into MRK could compress dividend yield and make the name vulnerable to volatility spikes if a single pipeline event disappoints.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.22

Ticker Sentiment