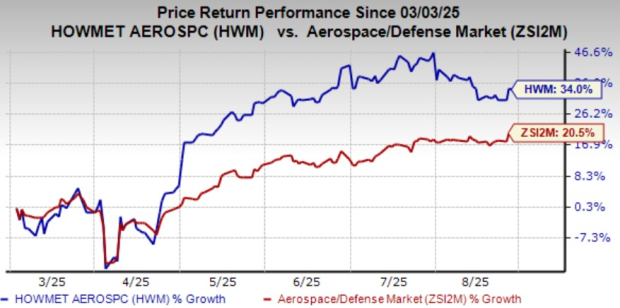

Howmet Aerospace (HWM) is navigating persistent weakness in its commercial transportation market, evidenced by Q1 and Q2 2025 revenue declines and rising cost of goods sold due to higher input costs and supply chain issues, with softness expected to continue through H2. This is partially offset by robust performance in its commercial and defense aerospace segments, driven by strong orders. Despite these headwinds, HWM shares have surged 34% in the last six months, and earnings estimates are rising, though the stock trades at an elevated forward P/E of 43.51x.

Howmet Aerospace (HWM) presents a bifurcated operational picture, with robust momentum in its aerospace business offsetting significant headwinds in its commercial transportation segment. The transportation division continues to struggle, with revenues declining 4% year-over-year in Q2 2025 following a 14% drop in Q1, a weakness management expects will persist through the second half of the year due to softer truck builds and tariff-related uncertainty. Concurrently, the company faces margin pressure from rising input costs, evidenced by a 7.3% increase in cost of goods sold in 2024 and a 3% rise in H1 2025, driven by higher aluminum prices and supply-chain volatility. This industry-wide transportation softness is corroborated by peer Kennametal's (KMT) performance. However, these challenges are being counteracted by strong demand in HWM's commercial and defense aerospace markets, fueled by robust orders for F-35 engine spares and airframe components, a trend mirrored by GE's record-breaking engine deals. Despite the mixed fundamentals, the market has favored HWM, with its stock surging 34% in the last six months, significantly outperforming the industry's 20.5% growth. This has pushed its valuation to a premium, with a forward P/E ratio of 43.51x, well above the industry average of 28.19x, suggesting investors are pricing in a strong aerospace recovery and looking past the near-term transportation and cost challenges.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

Moderately Positive

Sentiment Score

0.45

Ticker Sentiment