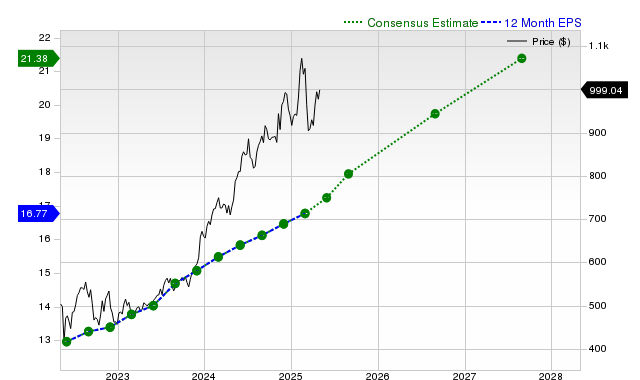

Costco (COST) is attracting investor attention, reporting consistent earnings and revenue growth forecasts, including a projected current quarter EPS of $5.80 (+12.6% YoY) and revenue of $85.93 billion (+7.8% YoY), with estimates remaining stable. Despite these positive fundamentals and a history of slightly exceeding consensus, the stock's recent performance has lagged the broader S&P 500 and its retail discount industry peers, and its Zacks Rank #3 (Hold) and 'D' valuation score indicate it trades at a premium and may perform in line with the broader market in the near term.

Costco (COST) exhibits a profile of steady fundamental growth juxtaposed with a rich valuation and lagging stock performance. The company's earnings outlook is robust, with consensus estimates pointing to a 12.6% year-over-year EPS increase for the current quarter and an 11.6% rise for the current fiscal year. This is supported by projected revenue growth of 7.8% for the quarter and 8.1% for the year. Historically, Costco has demonstrated reliability by beating consensus EPS and revenue estimates in three of the last four quarters, albeit by narrow margins. However, these positive fundamentals are tempered by several factors. The stock's +0.8% return over the past month has underperformed both the S&P 500 (+2%) and its direct industry group (+3.5%). Furthermore, consensus earnings estimates have remained unchanged over the last 30 days, suggesting a lack of new positive catalysts to drive analyst sentiment higher. This combination of factors is crystallized in its Zacks Rank #3 (Hold) and a 'D' grade for Value, which explicitly indicates the stock is trading at a premium to its peers and may only perform in line with the market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment