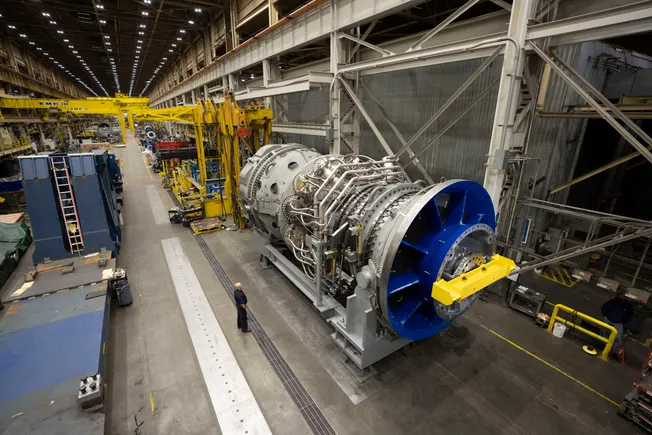

GE Vernova reported strong Q1 2026 order growth across all three segments, with electrification orders up 86% organically and backlog rising to $42.4 billion from $25 billion a year ago. The Prolec GE acquisition is already contributing about $500 million in incremental revenue and is expected to add roughly $3 billion to 2026 top line, while gas turbine backlog climbed to 100 GW from 83 GW at year-end 2025. Wind remains the weak spot, with revenue down about 25% and management citing permitting delays plus tariff uncertainty in the U.S.

The market is starting to re-rate GEV as a utility-grade infrastructure compounder, not a cyclical equipment name. The key second-order effect is that its electrification book is now becoming the lead indicator for grid capex across utilities and hyperscalers, while the Prolec consolidation effectively converts a previously shared economics stream into controllable margin and cash-flow leverage. That combination should keep multiple expansion alive even if power generation volumes normalize, because the market can underwrite a longer-duration backlog with better visibility on mix and pricing. The biggest beneficiary beyond GEV is the broader grid supply chain: transformer, switchgear, HVDC, and substation vendors should see a multi-quarter pricing tailwind as data center load growth collides with limited manufacturing capacity. This is also a negative for smaller private vendors and EPCs that lack balance-sheet scale; they will likely lose share on integrated projects where customers increasingly want one-stop power + transmission solutions. Conversely, wind remains a policy beta trap: even if order comparisons improve, U.S. developer demand looks too fragile to support a durable valuation rerate absent clearer permitting/tariff relief. The gas backlog inflection is more important than the headline order growth because it implies pricing power is still outrunning inflation while capacity stays tight through the end of the decade. That sets up a multi-year earnings stair-step, but it also creates the main reversal risk: if utilities slow commitments or data center hyperscalers defer load buildouts, the market may discount the outer-year backlog more heavily and compress the multiple. The near-term catalyst path is cleaner over the next 1-2 quarters than the wind story; the stock can keep grinding higher on backlog conversion and margin commentary, but any disappointment on install timing or working capital could be enough to pause the rerate. Consensus is likely underestimating how much of the story is now about transmission bottlenecks, not generation demand. If grid connectivity remains the gating factor, GEV can keep benefiting even in a softer macro because customers are forced to fund the interconnect and equipment layer first; that makes this one of the better ways to express AI/data-center power demand without paying up for pure software beneficiaries. The contrarian risk is that the market may be extrapolating all of this into 2027-2030 too aggressively, so the right framing is not a straight-line long, but long quality infrastructure with hedges against wind and execution disappointment.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.45

Ticker Sentiment