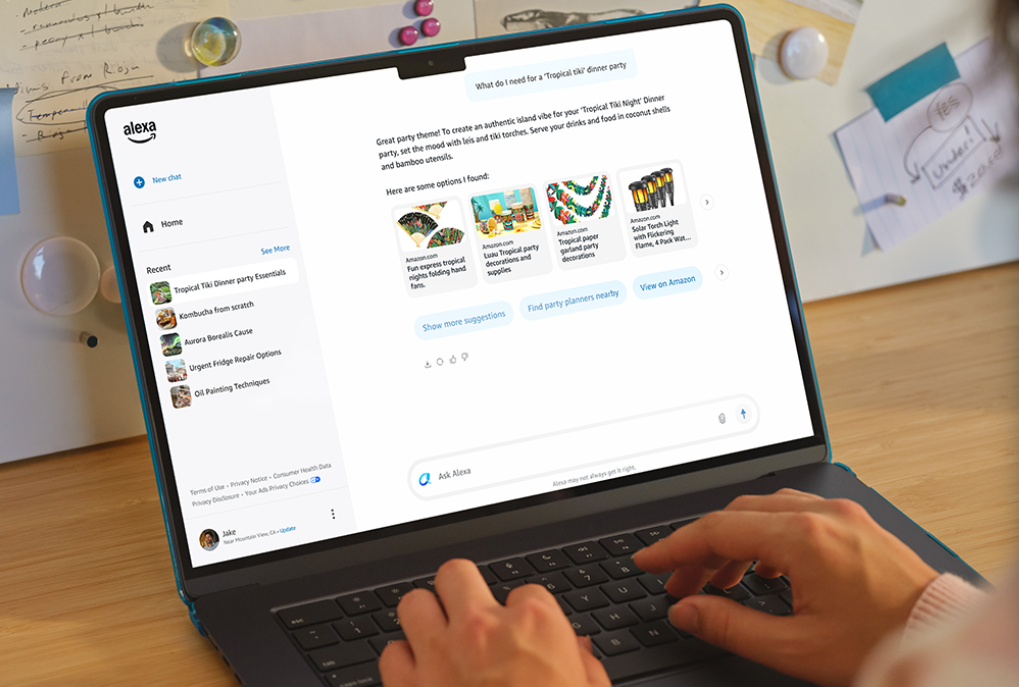

Amazon has rolled out Alexa+ on the web (alexa.com), expanding a generative-AI upgrade that previously launched on Android and iOS and maintains context across Echo and Fire TV. The assistant can plan events, book services and complete Amazon purchases; access requires either a $19.99 monthly subscription or is included with Prime, positioning Amazon to monetize assistant usage and compete directly with OpenAI's ChatGPT and Google Gemini while potentially boosting engagement and commerce conversion without immediate material impact to near-term financials.

Market structure: Alexa+ on the web accelerates Amazon's vertical linkage from query -> transaction; winners include AMZN (commerce, Prime retention, incremental subscription revenue at $19.99/mo) and AWS/AI infra suppliers (NVDA, INTC) if compute ramp follows. Losers are incumbent search/ad revenue capture (GOOGL) and standalone chatbot monetizers that lack buying integration. Expect modest pricing power for Amazon in voice-driven commerce: a 1–3% lift in conversion rate from voice could translate to $2–5B incremental GMV annually within 12–24 months. Risk assessment: Key tail risks are regulatory (antitrust tying of assistant to Amazon commerce in US/EU) and operational (model hallucinations causing refunds/reputational losses); assign ~10–15% probability of material regulatory action within 12–24 months. Short-term (days–weeks) impact is news-driven; medium-term (3–12 months) depends on adoption metrics (monitor paying users hitting 5M/12 months). Hidden dependency: AWS GPU supply and latency costs could compress margin if Amazon subsidizes model runs to seed adoption. Trade implications: Tactical: constructive on AMZN equity and capped-leverage long options for 6–18 month windows; consider pair trade long AMZN / short GOOGL to isolate commerce vs. search risk. Hedge with small long NVDA (0.5–1% portfolio) for infrastructure upside. Entry timing: initiate in tranches over next 4–8 weeks while watching Alexa+ paid subscriber cadence and Prime stickiness data. Contrarian angles: Consensus overplays immediate threat to Google; adoption velocity for transactional voice is slower — 6–12 months to meaningful monetization. Conversely, market may underprice regulatory fines: a single EU fine or mandated unbundling could cut valuation multiple by 10–20%. Watch user conversion thresholds (2% -> marginal, 5%+ -> disruptive) and regulator filings (90-day window) as binary catalysts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment